The chart of accounts is simply a list of all of the account types you might use when recording your business income and expenditure activities. The “account types” include assets, liabilities, equity, income, expenses, other income and other expenses. The accounts are separated like this for reporting purposes and are used to build the balance sheet and the profit and loss report. Business owners and accounting professionals use these reports to ascertain the financial health of the business. As a business owner, it is very important that you understand these reports. In order to to do this, you must first be across each of the account types found in the chart of accounts. Today, in this two-part blog, we look at these account types and explain what they mean and their accounting purpose.

There are seven account types residing within the chart of accounts. These include:

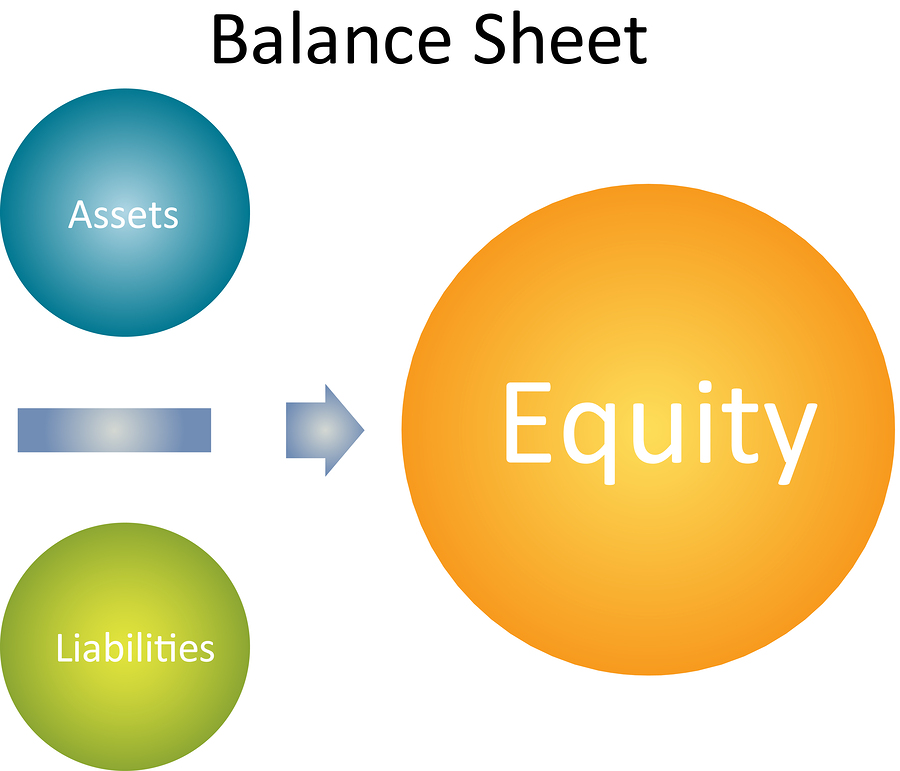

- Assets

- Liabilities

- Equity

- Expenses

- Income

- Other Expenses

- Other Income

For reporting purposes, the assets, liabilities and equity accounts are found on the balance sheet and the remainder of accounts fall to the profit and loss report. Today, in part one of this blog, we will dissect each of the account types related to the balance sheet.

ASSETS

Business assets are “capital” items that the business owns. These might include things like bank accounts, cash, computers, vehicles, buildings or land. For bookkeeping purposes, they are separated into sub-accounts depending on how soon they can be converted into cash. The sub-headings include:

- Current Assets

- Non-Current Assets (or Fixed Assets)

- Intangible Assets

Any assets that could be converted into cash within the next 12 months are categorised as “current assets”. These could be things like:

- Bank accounts and/or cash

- Short-term investments, like shares or unit trust holdings

- Accounts receivable – all of the money customers owe you

- Inventory – all stock or raw materials held by business for later on-sale to customers

Any assets owned that cannot be readily converted into cash within 12 months, are popped into the “non-current asset” category. These are things like:

- Land and buildings

- Plant and equipment – new computers, machinery, tools, furniture etc.

- Motor vehicles – any vehicle owned by the business

- Accumulated depreciation – the amount the accountant has claimed back in previous tax returns on non-current assets.

Other assets that are not readily converted into cash are known as “intangible assets”. These assets can’t be seen or touched, hence the intangible part. They include things like:

- Borrowing expenses – banking expenses related to a business loan

- Formulation expenses – expenses related to the setting up of a company

- Goodwill – usually part of the purchase price of a business

LIABILITIES

Liabilities are the all of the amounts your business owes to other stakeholders. They can include credit card accounts, supplier bills, GST, PAYG Withholding, Superannuation Guarantee, bank loans, loans from others, loans to buy assets etc.

Liabilities are separated into sub-categories just like the assets.

- Current Liabilities

- Non-Current Liabilities

Current liabilities are those which are due for payment within one year. These can include:

- Credit cards

- Overdrafts

- Accounts payable – money you owe to suppliers

- Other – customer deposits, short-term director loans

- GST

- PAYG Withholding

- Superannuation Guarantee

Non-current liabilities are those items which are not due to be paid within one year and can include:

- Bank loans

- Loans from others – money loaned from family or friends

- Hire purchase or chattel mortgage – often vehicles and office equipment is purchased via these types of loans.

EQUITY

Put simply, the result of subtracting liabilities from assets is known as “equity”. This is the “interest” a director, shareholder or business owner has in the business. Equity is made up of capital contributed and the profit and loss built up over time.

There are different equity accounts used for each business structure. These are outlined below:

Sole Trader

Equity accounts for sole traders can include:

- Owner’s capital – contributions made by owner

- Owner’s drawings – personal spending

- Current year’s profits (or loss) – the net profit or loss (taken from the Profit and Loss report).

Partnership

Equity accounts for a partnership can include:

- Partner’s capital – there needs to be one for each partner

- Partner’s drawings – again, there should be one for each partner

- Distribution of profit – the accountant writes profit distribution for each partner to this account at the end of the year.

Companies and Trusts

The main equity accounts for companies and trusts include:

- Retained earnings – income retained by a company that isn’t distributed to shareholders. These earnings or losses build up from one year to the next.

- Current year’s earnings

- Dividends paid – if shareholder receives a profit distribution, this payment is recorded here. For trusts, this account is known as “Trust Distributions Paid”.

- Shareholder capital – this is the value of all shares issued. This is known as “Issued Ordinary Units” in a trust structure.

So that’s the low-down on the balance sheet account types! Hopefully, you now have a clearer understanding of them. Next week we’ll look at the profit and loss accounts i.e. income, expenses, other income and other expenses. In the meantime, you can download our ready-made charts of accounts for all business structures – they’re free! Until next time, happy bookkeeping!

Thanks Louise. Great post. Very easy to understand…

Hey Louise, good post but you may want to list Cost of Good Sold also as a separate account group between Income and Expenses. Very Important for Business Owners who want to keep track of GP margin.

Hi Kerry, thanks for commenting. I cover off Cost of Goods Sold in part 2 of this blog. See here https://www.e-bas.com.au/bookkeeping-blog/chart-of-accounts-explained-part-2

Hope that helps.

Great explanation of the chart of accounts! I really like how you broke down the balance sheet categories like assets, liabilities, and equity. Understanding how these accounts are structured makes it much easier to read financial reports and track overall business health.

Thank you. That’s a nice comment!