What NOT to include in payslips for paid Family & Domestic Violence Leave

Here is a reminder that access to paid family and domestic violence leave for employees of non-small business employers (employers with 15 or more employees) began on 1st February 2023 (and 1st August 2023 for small business employers). The leave is for 10 days for any full, part-time or casual employees and is not pro-rated. Read more about this new leave type in our previous blog here.

Something important to call out in relation to paying this leave is the information that is prohibited from being included on the employee’s payslip.

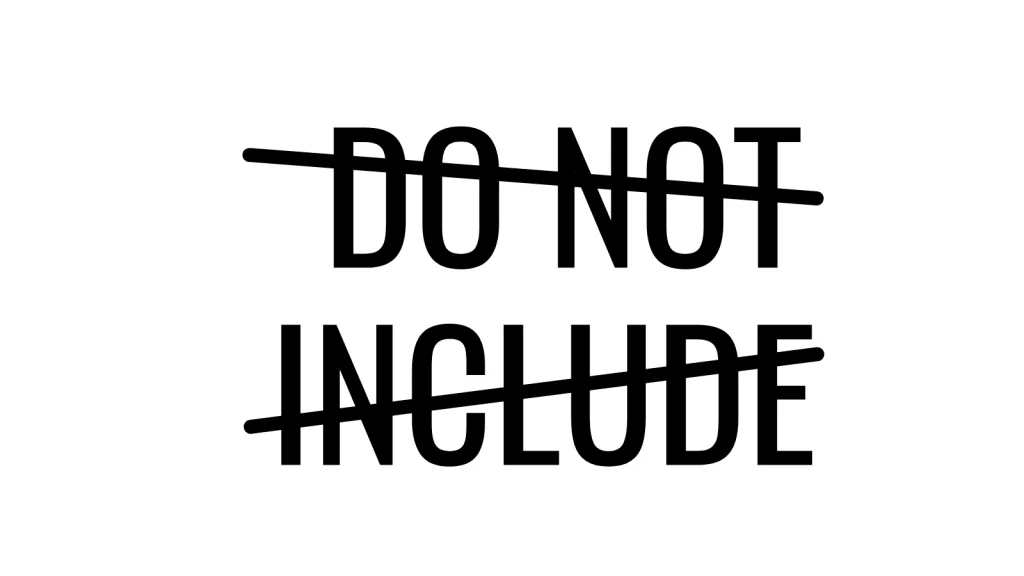

Employers must not include:

- A statement that an amount paid to an employee is a payment in respect of the employee’s entitlement to paid family and domestic violence leave

- A statement that a period of leave taken by the employee has been taken as a period of paid family and domestic violence leave

- The balance of an employee’s entitlement to paid family and domestic violence leave

The reason for not including this information is that if a perpetrator of violence gains access to the employee’s payslip and sees that this type of leave has been taken, this may pose a significant risk to the employee.

When setting up this type of leave in the payroll system, it is important to give it a generic name that does not reference the words “Family and Domestic Violence Leave”. In fact, not calling it “leave” at all is best practice. Given the payment is for an employee’s full rate of pay for the hours he/she would have worked if they weren’t on leave, then simply producing a payslip that shows “gross” pay, is recommended. In the back end of the payroll setup, details can be added noting what the payments actually are, and leave entitlement balances can be recorded but not included on the payslip (simply uncheck that box in the employee’s payroll setup (software-dependent)).

Precluding statements about this type of leave on an affected employee’s payslip is now part of the Fair Work Legislation Amendment Regulations 2022. Employers must take note and ensure that their payroll systems are set up correctly to reflect these amendments. Failing to do so may/will put affected employees at significant risk. If you are an employer, make sure you action this now (or by August 2023 if you are a small employer).

What NOT to include in payslips for paid Family & Domestic Violence Leave Read More »