Payday Super is a government reform that will require employers to pay Super Guarantee contributions on or soon after each payday, instead of making contributions quarterly or monthly. The new rules begin on 1 July 2026. The intent is to reduce unpaid/late super, give employees more timely contributions into their funds, and give the ATO closer to realtime visibility of employers who fall behind.

This dashboard has been created to provide employers with resources and insights to help them understand Payday Super and prepare for its impact. Use the dashboard to navigate Payday Super rules and prepare your business for the transition.

Note: As of March 2026, legislation and regulations relating to Payday Super are still in the process of being finalised by Treasury and the ATO. The information provided in this dashboard will be updated as and when the details are finalised.

The Australian Government has passed the Payday Super legislation and it has received Royal Assent. Payday Super will take effect from 1 July 2026. This new law requires employers to pay superannuation guarantee (SG) contributions on payday and ensure that funds reach employees’ super accounts within seven business days, instead of quarterly or monthly. If you’re an employer, this blog will help you understand how Payday Super will affect your payroll processes.

What employers need to know

Payment Timing:

1. Super must be paid within seven business days of each payday.

2. If a new employee is hired or an employee changes their super fund, first-time payments must be received by the fund by the end of the 20th business day and after each payday.

3. Super on out-of-cycle or bonus payments may be included in the next regular pay cycle, however this does not apply to the termination of employees.

4. The ATO May extend time-frames for events such as natural disasters or systems outages.

Qualifying Earnings: The law introduces the concept of ‘qualifying earnings’ for super calculations. This concept will replace the dual “salary or wages” vs “ordinary times earnings” model. One qualifying-earnings base will simplify administration. It is important to note that amounts which are salary sacrificed to a superannuation fund count toward qualifying earnings and cannot offset required SG.

Maximum Contributions Base (MCB): The maximum contributions base will now be an annual limit, as opposed to quarterly. The calculation will be Concessional Cap x 100 divided by the current SG rate i.e. $30,000 x 100 divided by 12 = $250,000.

Stricter Penalties: There are tougher penalties for late or missed payments. As per current rules, should contributions be missed or paid late, a penalty known as the Superannuation Guarantee Charge (SGC) is created which includes interest and penalties. This won’t change under Payday Super rules, however the penalties will be more robust including:

Administrative uplift: 60 % of unpaid amounts (may be reduced by regulation);

Late-payment penalties: 25% – 50% of outstanding charge if not paid within 28 days of notice;

Additional ATO penalties: up to 200 % for repeated or unreported breaches.

Tax Deductibility: Late contributions and the SGC will be tax deductible. However, any late payment penalties related to the SGC will not be deductible.

Onboarding: The process for onboarding new employees will need to be more streamlined in order to minimize fund rejection errors, such as incorrect employee master data and choice of fund information. Employers need to consider automated solutions to replace manual processes.

What employers should do now

Update Payroll Systems: Ensure your payroll software can process super payments on every payday. Also ensure that the super funds you pay are ready for Payday Super.

Educate Staff: Inform payroll and HR teams about the new requirements. Also inform your employees.

Review Staff Contracts: The advent of Payday Super will require changes to the wording in employee contracts. It may also affect remuneration for some employees – this requires close scrutiny and review.

Monitor Compliance: Regularly check that payments are made on time to avoid penalties. Running some test scenarios prior to the advent of Payday Super would be prudent. This would allow employers to iron-out the kinks and deal with potential bottle necks and issues.

Change to Payday super Now: You don’t have to wait until Payday Super begins in July 2026. You can start doing it now as long as your processes and software are up to par. If you start now, you will be able to ensure that all or any issues are removed before Payday Super becomes compulsory.

My opinion

Because it is a pet-hate of mine when employers don’t pay employees’ super on time (or at all), I am 100% in support of Payday Super. This new law will ensure that super gets into employees’ super accounts on time and regularly, rather than quarterly, or longer, or sadly, not at all. More regular super payments will see employees’ super balances increase due to higher interest accrued. All good in my book.

I do note, however, that there will be logistical issues such as the super funds not processing the payments within 7 business days and employers paying the super towards the latter end of the 7 day period. This in turn could expose employers to late payment penalties which may occur through no fault of their own. The tight processing time-frame is definitely going to be a problem.

There will also be cash flow issues for employers. Employers will need to ensure that they have enough funds on hand to pay super on payday, from 1 July 2026 and for each and every payday going forward. The current 3 month grace period will be no longer which could put many employers under considerable cash flow stress. Management of cash flow will become extremely important.

Another issue could lie with software companies not being ready to cope with these changes by 1 July 2026, given this is only 7 months away! This is unlikely, but definitely possible.

Lastly, those employers who outsource the processing of payroll will be hit with higher charges due to the extra administration required on payday to process super payments. What would have been a quarterly or monthly job will now become a weekly, fortnightly, bi-monthly, etc. job, depending on the pay cycle used. This aspect will also affect employers’ cash flow!

Payday Super won’t be without its hiccups, but I do believe it will vastly improve the superannuation system, ensure employees are better off, and stop rogue employers from ducking and weaving when it comes to paying employees’ super.

Key Takeaways

The Australian Government passed the Payday Super is law, requiring employers to pay superannuation contributions on payday from 1 July 2026.

Employers must ensure super payments are made within seven business days and streamline onboarding processes to reduce errors.

The new law introduces ‘qualifying earnings’ for super calculations and a stricter penalties regime for late payments.

Employers should update payroll systems, educate staff, review contracts, and monitor compliance ahead of the change.

Despite potential cash flow issues and logistical challenges, the Payday Super law aims to improve employee superannuation outcomes.

Every year, as we approach the Christmas break, I like to remind employers and employees about their rights and responsibilities in terms of taking leave and how this relates to public holidays. This blog will address this issue and help you all plan your payroll for the upcoming festive season.

All businesses are different and have varying requirements during the festive season. Some shut down completely, while others remain open, even on public holidays.

Shutdowns

If your business shuts down at Christmas, you can give your employees the direction to take annual leave for the shutdown period. Your direction must be reasonable, in writing, and provided to all affected employees. If your employees are covered by an award or enterprise agreement, you do need to check the rules relating to shutdown and directing employees to take leave, because all awards and agreements are different. If no award or agreement applies, employers can only direct the employee to take annual leave if the direction is reasonable.

Employees without enough accrued annual leave

Sometimes, employees may not have accrued enough annual leave to cover the full period of a shutdown. In this case, employers can agree to allow an application for annual leave accrued in advance or for unpaid leave. Whatever is decided, it is important to check the rules in the award if one applies, and to put all decisions made in writing.

Working during the festive season

If your business remains open during all or some of the festive season, the rules for taking and paying leave are fairly simple. Workers need to receive their normal pay while they work and be paid for any public holidays that they take off. If they work on a public holiday, workers need to be paid public holiday rates which are listed in all awards.

Employers may request that workers do overtime during the festive season, including on public holidays. However, this request must be reasonable, taking into consideration the needs of the business and the employees’ personal commitments. Again, this is driven by the relevant award and/or the employees’ contract, if they are award-free. Remember, if employees work on a public holiday and do overtime on that day, they may be eligible for penalty rates, another day off or extra annual leave – check your award to clarify the details.

Not working on a public holiday

If an employee doesn’t work on a public holiday, they must be paid their base rate for the ordinary hours they would have worked. Public holidays are not deducted from the employee’s accrued leave balance, so ensure that all leave applications do not include any public holidays before approving them. These rules also apply during a shutdown. It’s important to note that employees should be given the choice to work on a public holiday, should they wish to do so.

Employers can direct employees to take annual leave during shutdowns, but the direction must be reasonable and in writing.

If employees lack sufficient accrued annual leave for a shutdown, employers can grant unpaid leave or annual leave in advance with proper documentation.

Employees working during the festive season must receive normal pay, and those working on public holidays need to be compensated at public holiday rates.

Employees not working on a public holiday should receive their base hourly rate for hours missed, not affecting their accrued leave.

Consult relevant awards and agreements for specific leave entitlements and payroll guidelines during the festive season.

For small business employers and their employees, Australia’s new Right to Disconnect Laws became effective on August 26, 2025. These laws will empower employees to switch off from work outside of their regular hours, enabling them to achieve a better work-life balance. Having the right to disconnect means employees can refuse to answer calls, emails, texts, and other messages from their employer or third parties—like clients, customers and suppliers —unless the request is unreasonable.

Watch the below video from Fair Work for an indepth overview of the Right to Disconnect Laws for Small Businesses:

Crafting a Fair Policy

The Right to Disconnect laws require every business to review how team members communicate with each other and more specifically, when. It is best practice once this review is completed, to create a clear and effective Right to Disconnect policy that all team members will follow. Since the expectations for after-hours contact can vary greatly depending on employees’ positions, it is crucial to have open conversations and document the agreed-upon standards. The policy should define what reasonable and “unreasonable” contact means for a specific workplace and individual roles.

Regularly reviewing and updating this policy will help ensure it continues to support both the business’s needs and the well-being of its employees.

As a bonus for those who are reading this post, I have created a Right to Disconnect policy template. Download it for free below.

The following video from Fair Work, provides information about having discussions with employees about these new laws. These “discussions” will assist in crafting a policy that best suits the needs of the employees, and will help them understand their rights and those of the business.

For more information about the Right to Disconnect and to view examples, visit this Fair Work webpage.

In this blog I will show you how to set up a fully serviced novated lease for a motor vehicle in Xero. Before I begin, I would like to make it clear that every novated lease arrangement is different, depending on the agreement made between the employee and the lease provider. If this “how to” does not seem to match up with your requirements, please seek further advice from your tax agent or the lease provider. I will not be providing advice to readers about their individual requirements for their novated lease set ups, so please don’t ask! Again, seek advice from your tax professional or the lease provider company if you need help.

What is a Novated Lease?

Before diving into the “how-to” of this blog, it’s important to understand what a novated lease is. A Novated lease itself is a type of vehicle financing arrangement involving an employee, their employer and a leasing provider. Essentially, an employee is able to purchase a vehicle AND receive tax concessions under a salary sacrifice arrangement, orchestrated through payroll. Simply put, “to novate” means “to move with,” and in the context of a novated lease, it signifies that the employee’s vehicle and lease agreement can move with them if they change employers.

How a Novated Lease Works

Basically, a novated lease occurs as per the below steps:

An employee chooses a vehicle to buy.

A Leasing Provider provides a lease agreement to the employee which sees the employer take over the rights and obligations under the lease via a “deed of novation”. It should be noted that the deed of novation includes a clause that transfers the lease obligations back to the employee on termination of the lease or when the employee ceases employment with the employer.

The employee and employer enter into a salary sacrifice agreement whereby deductions are taken from the employee’s pay to fund the lease.

The employer pays the leasing provider with the payroll deduction funds. This means the employer is not out of pocket, both from a cash flow and tax perspective.

What is a Fully Serviced Novated Lease?

In this scenario, another party is introduced – a salary packaging provider. This provider will send the employer a reconciliation report the compares the actual motor vehicle costs against the novated lease estimated costs. If there is any variance, an adjustment must be made to the employee’s pre-tax deduction and sometimes, an adjustment is also required to the post-tax deduction.

A fully serviced novated lease includes, not only the lease repayments, but also other vehicle expenses such as:

Insurance

Maintenance like servicing, repairs and parts

Registration

Fuel

Roadside Assistance

Tolls

Car washing

This type of novated lease operates in the same way as described above, however it has an extra component which is FBT. The post-tax deduction is known as an Employee FBT Contribution which attracts GST. The employer also claims the GST on the novated lease expenses. The pre-tax deduction is calculated as the novated lease expenses minus the post-tax deduction (GST exclusive).

How to Set up the Fully Serviced Novated Lease in Xero

This “how to” will be based on the following novated lease example:

Sonia works for ABC Industries and is paid $120,000 plus super per annum on a monthly pay cycle. She decides to purchase a vehicle costing $60,000 and asks her employer if she can salary sacrifice the purchase via a fully serviced novated lease. Sonia’s employer agrees with the request and asks Billy’s Novated Lease Services to assist with the facilitation of the lease. Once the lease is in place, Billy’s Novated Lease Services provides the following information to ABC Industries:

The novated lease will be for 5 years and based on the following estimated costs, the fixed monthly amount will be $2,017.08. See the details below:

ITEM

GST Exclusive

GST

TOTAL

Lease Payment

14,000

1,400

15,400

Fuel

3,000

300

3,300

Servicing & Repairs

2,000

200

2,200

Registration

900

0

900

Insurance

1000

85

1085

Roadside Assistance

500

50

550

Tolls

400

40

440

Car Wash and Vacuum

300

30

330

TotalEstimated Annual Costs

22,100

2,105

24,205

Monthly Novated Lease Amount

1,841.66

175.42

2,017.08

The fringe benefit figure and related pre and post tax figures are also provided to ABC Industries as below:

The following steps will need to be actioned in order to set up the above lease in Xero:

Step 1 – Add the following accounts to the Chart of Accounts

Novated Lease Clearing Account – liability account, current liability; – BAS Excluded tax code; set up a separate account for each affected employee.

Novated Lease Expenses – expense account – BAS Excluded tax code; put under payroll costs like wages or super etc.

Employee FBT Contributions – revenue account – GST on Income tax code; place under non-trading income type e.g. “Other Income”

Fringe Benefits Tax – needed if an FBT liability arises; expense account – BAS Excluded tax code; place under general overheads.

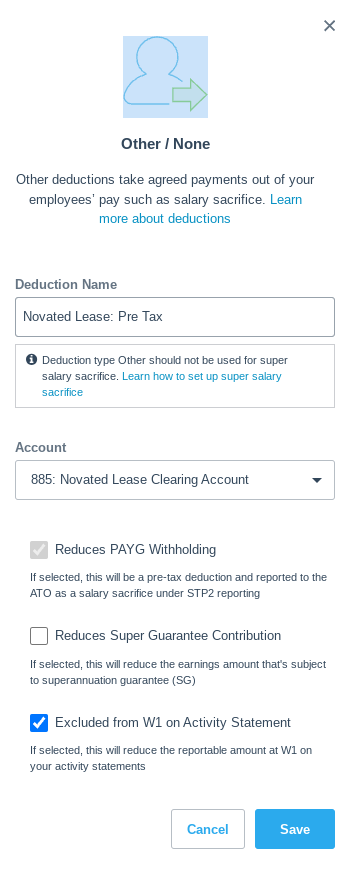

Step 2 – Set up the payroll tax deductions

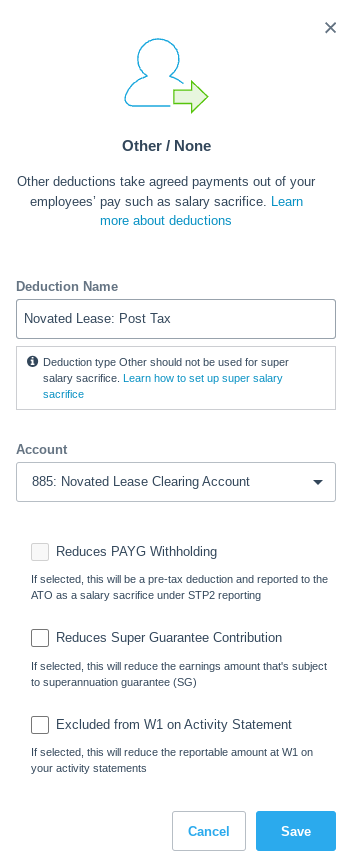

Pre-Tax Novated Lease Deduction – reduces PAYG WH; may or may not reduce SG (but shouldn’t); excluded from W1; STP – Salary Sacrifice – Other Employee Benefits (type O); direct this deduction to the Novated Lease Clearing Account.

Post-Tax Novated Lease Deduction – Does not reduce PAYG WH; Does not reduce SG; Is not excluded from W1; STP – not reportable; direct this deduction to the Novated Lease Clearing Account.

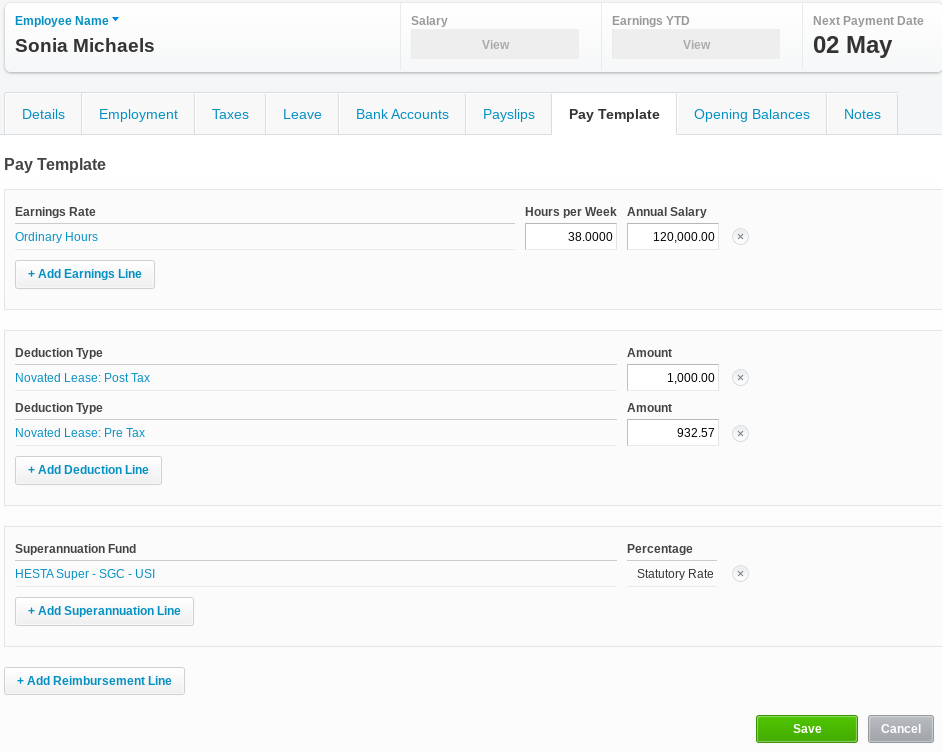

Step 3 – Set up the employee’s pay template & run a pay cycle

Open Sonia’s pay profile in Xero. Add the two deductions as above, then enter the figures provided by the lease provider. See below:

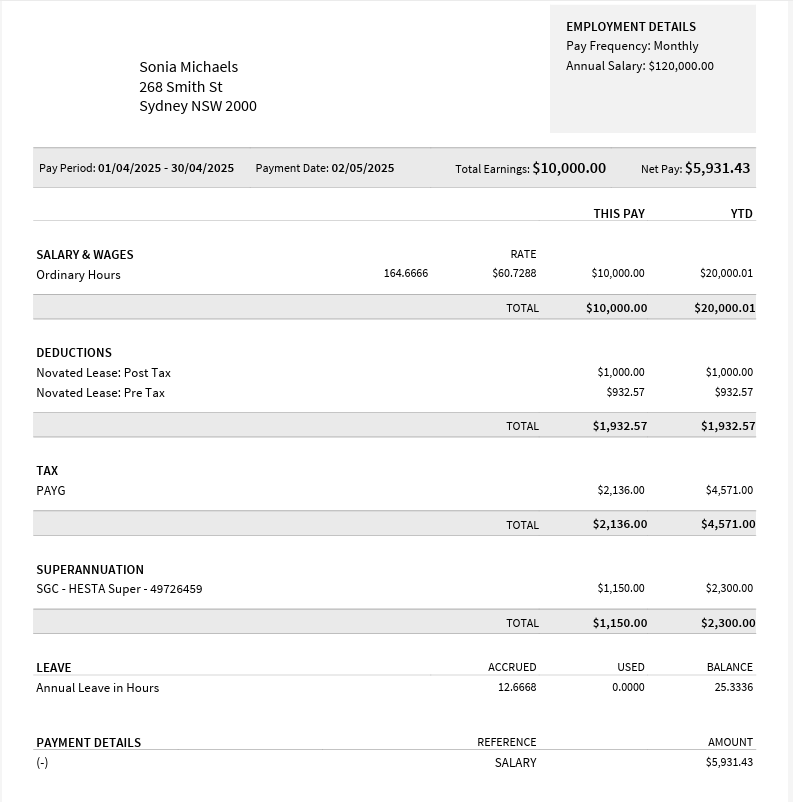

Now process the April pay run in Xero. Sonia’s payslip should look like the below example:

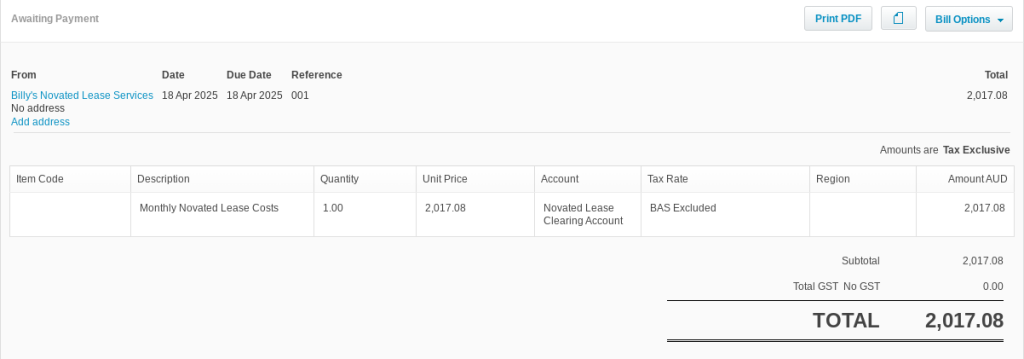

Step 4 – Record the lease provider’s invoice in Xero

In Xero, add the invoice received from the lease provider, “Billy’s Novated Lease Services”. Post the invoice to the Novated Lease Clearing Account with the BAS Excluded tax code. See an example below.

Step 5 – Record GST

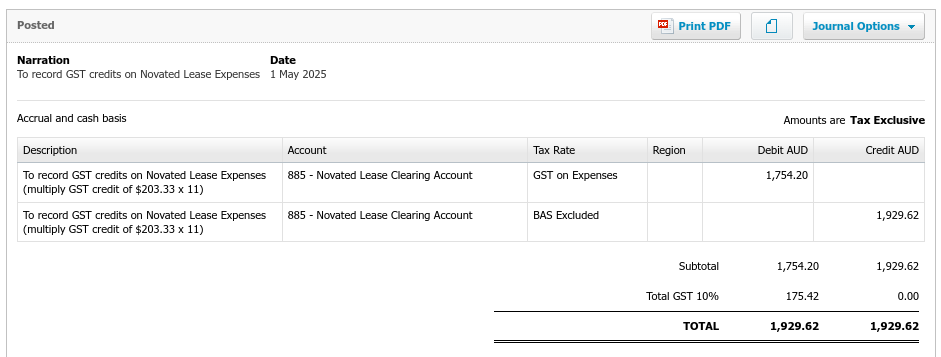

There are two GST-related transactions to bring to account:

GST on the novated lease expenses

GST on the post-tax deduction

Each month, Billy’s Novated Lease Services will send ABC Industries a report detailing any GST credits available from the novated lease arrangement from the previous month. For ease of explaining this “how to”, we will assume the GST credits align with the example data. The GST credit therefore is $175.42. Now multiply the GST by 11. This will give rise to a figure of $1,929.62. To recognise the GST from the monthly report, enter the following journal:

Here, GST of $175.42 will move to the GST control account and become claimable in the BAS. The clearing account will receive net credit of $175.42.

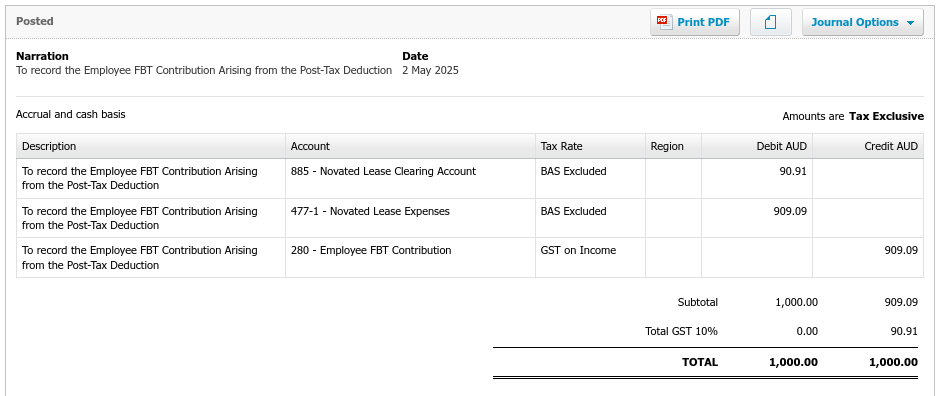

In order to take up the GST from the post-tax novated lease deduction i.e $90.91, enter the following journal:

The consequences of this journal will be:

$90.91 is credited to the GST control account;

The Novated Lease Clearing Account receives a debit of $90.91; and

Novated Lease Expenses receives a debit of $909.09.

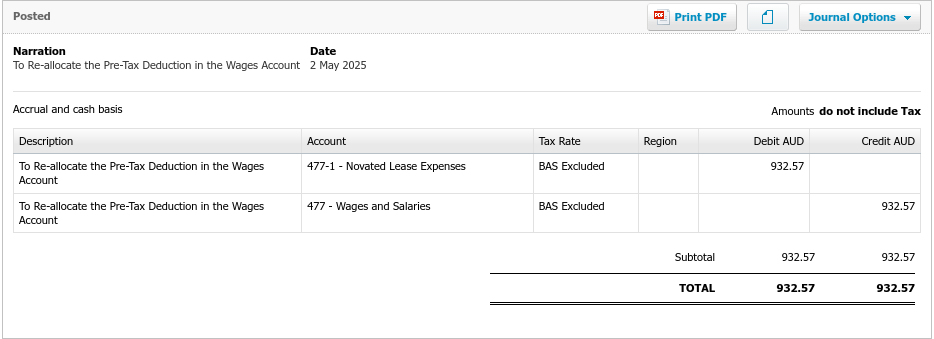

Step 6 – Correct overstated wages

The above payroll event has resulted in overstating the gross wages in the profit and loss. This is corrected by entering the following journal:

Behind the scenes – how are the accounts and the BAS affected by the novated lease?

Now that the above transactions have been processed in Xero, it would be prudent to show you how they affect the accounts and the BAS. Firstly, the novated lease clearing account has been cleared to zero as can be seen below. The account should return to zero each month after the payroll has been processed. If it doesn’t, you will need to investigate to find the cause!

The profit and loss shows the employee FBT contribution as other income and the lease and wage expenses are listed as expected:

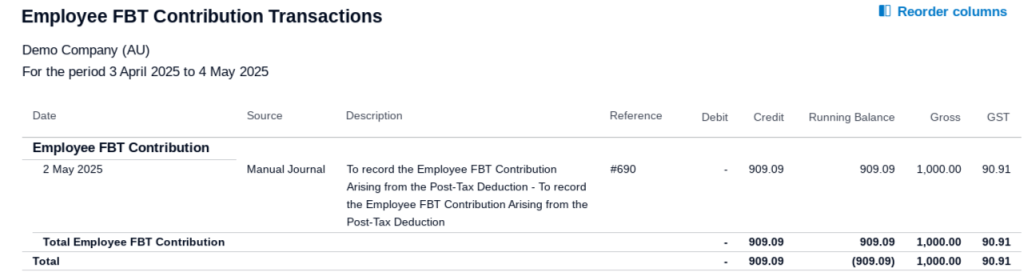

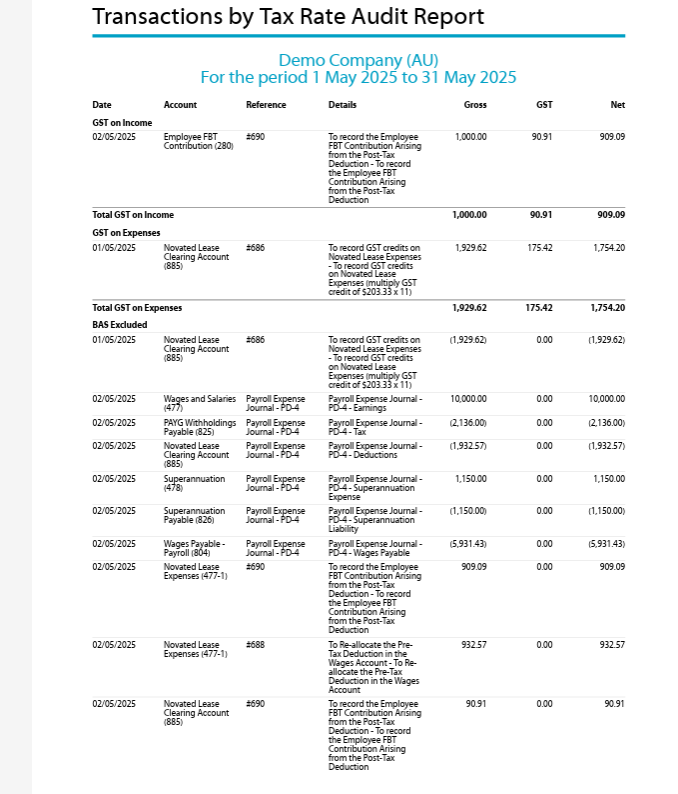

Now let’s drill into each profit and loss account to see the details. Looking at the FBT income I recorded at step 5, we can clearly see the GST posted of $90.91.

Next we can see the details behind the novated lease expenses recorded at step 5 and step 6. The total agrees with the monthly GST exclusive expense amount estimated by the lease provider.

Lastly, looking behind the wages expense transactions, we can clearly see how the wages are reduced by the reallocation of the pre-tax deduction:

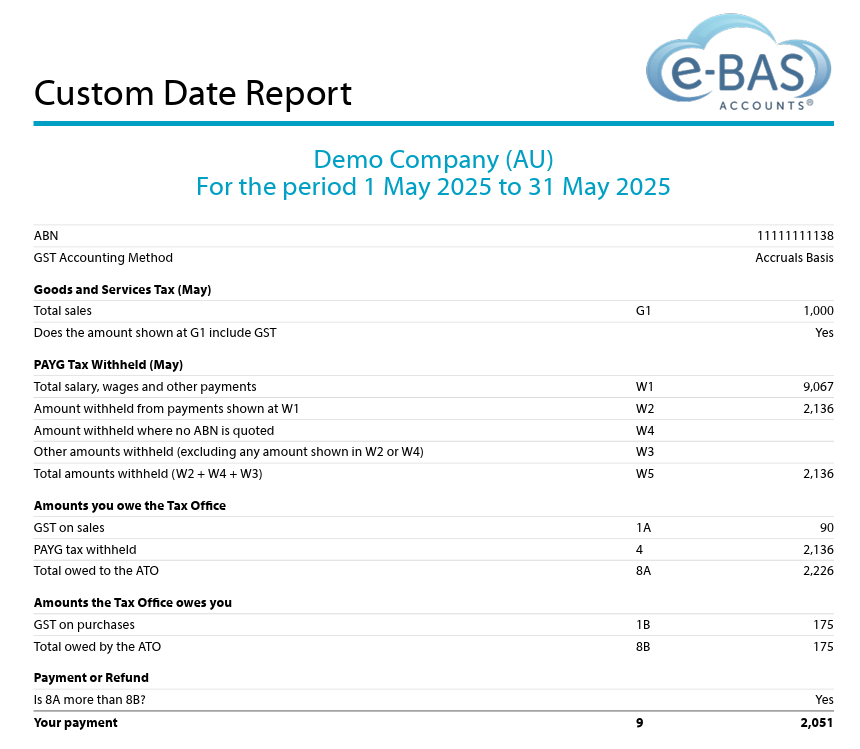

Now we will take a look at the BAS. Note the GST on sales of $90 from the FBT contribution and the GST on Purchases of $175 from the novated lease expenses journal. Also note the reduced gross wages figure which is the correct figure to report to the ATO.

Drilling down into each GST type below, shows us the origin of the figures:

Summary

Setting up a fully serviced novated lease in Xero, as outlined in this guide, offers one approach to managing these arrangements. It’s important to remember that variations in novated lease structures exist, each with its own implications for employee wages and payroll processing. While the data you receive from your lease provider might differ from the steps detailed here, this ‘how-to’ should provide a solid foundation for establishing the necessary accounts and configuring tax deductions within Xero. Please note that I cannot offer guidance on your specific lease agreement, however, I’m happy to address any questions you have about the instructions provided in this blog. Finally, the example figures used in this guide are purely illustrative and should not be evaluated for their financial accuracy or feasibility. The primary goal here is to demonstrate the mechanics of setting up a novated lease within Xero, so please focus on the procedural steps rather than the example’s specific details.

New Criminal Underpayment Laws began on 1 January 2025. It is now an offence to underpay your staff. If found guilty, you may face hefty fines or jail time, or both. Read on to find out what these laws mean and how you can avoid a conviction going forward.

What are these laws?

Employers found to be intentionally underpaying staff by Fair Work, will be investigated. If a case can be raised, it will be referred for criminal prosecution. If an employer is convicted, he/she may face prison time and/or fines (see below).

Employers who have made an honest mistake and did not intend to underpay staff, will not be prosecuted.

How to protect yourself

Fair Work has created the Voluntary Small Business Wage Compliance Code. This Code can be used to check if you are paying your staff correctly. Employers who have complied with the Code in relation to an underpayment, cannot be referred for possible criminal prosecution by Fair Work. Therefore, if you suspect that you may have underpaid staff, it is in your best interests to review the above Code ASAP!

Another way to protect yourself is to write an Cooperation Agreement. This is an agreement between Fair Work and an employer that outlines a possible underpayment event. While the agreement is in force, Fair Work cannot refer the matter for possible criminal prosecution, however, civil enforcement may apply regardless.

Which fines and prison time can apply?

For a company

If the court can determine the amount of the employer’s underpayment, the maximum fine will be the higher of:

3 times the amount of the underpayment

$8.25 million.

If the court can’t determine the amount of the underpayment, the maximum fine is $8.25 million.

For an individual

The court can impose a maximum of 10 years in prison or a fine, or both.

If the court can determine the amount of the employer’s underpayment, the maximum fine will be the higher of:

3 times the amount of the underpayment

$1.65 million.

If the court can’t determine the underpayment, the maximum fine is $1.65 million.

How to avoid all of the above

Simple really! Good employers do two things:

1. Stay up to date with payroll obligations including changes to awards, legislation and employees’ circumstances such as their roles, duties, classifications, relevant qualifications, age, hours of work or location of work.

2. Reach out to reliable sources for help when difficult payroll situations arise. These may include bookkeepers, tax agents, payroll HR associations, payroll processing services, industrial associations and Fair Work.

If you are reading this and are concerned about your situation, now might be the time to reach out to your tax professional and ask for assistance. Fair Work mean business!!

Late edit:

Fair Work have released their long awaited Payroll Remediation Guide. You can download it here. This Guide is directed more to larger employers, where a large number of underpayments or number of impacted employees are identified, or where the issues detected are complex and involve multiple industrial instruments.

Payday Super is coming! Payday Super aims to stop employers from not paying employees super or paying it late. The premise is that super will need to be paid after each pay run, even termination pay runs. Payday Super is set to begin from 1 July 2026.

Two proposed models for Payday Super implementation are:

“Employment payment” model: Employers must pay SG contributions on the same day as wages.

“Due date” model: SG contributions must reach the superannuation fund within a specified time after payday.

Both depend on the definition of “payday,” which includes any payment with an ordinary time earnings component, even outside the regular pay cycle like termination payments or bonuses. SG contributions would be calculated based on the ordinary time earnings paid on payday.

Payday Super will have specific impacts on the Super Guarantee Charge process and the maximum contribution base calculations. The government will consult with key stakeholders and the public to ensure these impacts are minimal.

The Government will finalise the Payday Super framework in the 2024–25 Budget. Legislation will be introduced for the measure set to begin on 1 July 2026. The ATO is consulting and co-designing with digital service providers for implementation.

In the meantime, employers must consider how Payday Super will affect their payroll processes and cash flow. It is also important to note that by July 2026, the super rate will be 12% which will also impact business cash flow. There are lots of issues to consider here and I will keep you updated as more information about Payday Super comes to hand.

Note: The government has released draft legislation to mandate payday super, a policy that was first flagged in the 2023-24 Federal Budget.

You may have heard that Payday Super is coming in July 2026. In short, Payday Super will require all employers to pay their employees’ super on the same day as a pay run is processed. The main reason behind this measure is that the Government wishes to end non-payment and underpayment of super by some employers as this is effectively wage theft. The measure will also mean that millions of employees will receive higher retirement savings due to their super contributions being paid earlier and more frequently.

What you may not know is that from 1 July 2026, the ATO Small Business Super Clearing House (SBSCH) will close. Yes, you heard right—it is closing its doors at the same time as Payday Super begins.

So, what can you do to prepare if you are a current SBSCH user? Your options are limited. You can either move to your default super fund’s clearing house or use the super functionality in your payroll software, such as Xero, MYOB, or QBO. I recommend not waiting until the SBSCH closes to get this organised. Make the change as soon as practicable.

How did I hear about the SBSCH closing? I read the fact sheet from the Government Treasury website. You can access the fact sheet here if you wish to read the details behind Payday Super.

The fact sheet breaks down many other details about Payday Super and is an important read if you are an employer. I suggest you take the time to review it and figure out how you will apply this change to your payroll processes when the time comes.

Good news has arrived for those planning a family in the next year or so. The government has decided to pay super guarantee equivalent payments on government-funded Paid Parental Leave (PPL). This will begin from 1st July 2025 i.e. for any babies born or adopted on or post this date. This measure is now law.

While Services Australia will continue to facilitate the PPL process, the ATO will be responsible for paying the super component (not employers). The ATO will pay the super in a lump sum at the start of the following financial year at the then super rate of 12% plus any interest owing. The first payments will be processed in July 2026.

This is a step forward in ensuring that those who choose to be stay-at-home parents are not disadvantaged in terms of future retirement savings. This is a good thing! A fairer system for all!

If a super payment has failed, the payment authoriser will receive an email notification, outlining the reason for the failure. The status of the payment will change from “pending processing” to “failed”. When this happens, the payment can be reprocessed as the batch will become available for selection in the “Add Super Payment” screen again. Details of the steps required to reprocess failed payments can be found in the above link.

Returned Auto Super Payments

As for failed payments, the authoriser will receive an email if a super payment is returned with information about which employees are affected. Xero can’t tell you why the payment was returned so you will have to contact the super fund affected to obtain those details.

In Xero, the payment status will change to either “partially returned” or “returned”, depending on how many employees are affected.

To find out how to reprocess returned auto super payments, go to the link above.

My Thoughts?

I think this update is an improvement overall, however, the following details from the above link about the timing of the status change to “failed”, have me a bit concerned:

‘This can take up to five business days, with further delays during peak processing times, such as at the end of a quarter. While waiting for the failure message, you can’t update the status of the batch manually.’

Given that the ATO states that “contributions are considered ‘paid’ when they are received by the super fund not when they are paid to the commercial clearing house”, the delays as described by Xero could trigger a Super Guarantee Charge requirement depending on the payment dates involved. This will adversely affect the employer and his/her cash flow, given the SGC increases the super liability overall. This seems a little unfair especially if the employer did pay the SG in a timely manner (or thought he/she did!).

I guess, the only remedy here is to ensure that SG is paid as early in the month as possible so that if any payments are returned or fail, they can be rectified well before the super payment cut-off dates. This issue will become null and void of course, when Payday Super begins (I hope!).