If you’re an employer, your PAYG withholding (PAYGWH) cycle might change depending on how much you withheld in the prior financial year. The ATO will advise you about this change in April each year via a written letter. The cycle change will occur on 1 July of the next financial year.

As a small withholder (small employer) you pay PAYGWH with GST and other taxes in your quarterly BAS. But, the ATO can switch your PAYGWH to monthly if, in the last financial year,

you withheld $25,001 to $1,000,000 from employee wages

These employers are called “medium withholders”.

If that’s you, you must lodge and pay a monthly Instalment Activity Statement (IAS) by the 21st of each month. For example, PAYGWH for July is due by August 21st.

If you withheld over $1 million last financial year, you’re a “large withholder”.

Large employers have specific dates to pay PAYGWH and get special payment reference numbers (PRN). The ATO will provide you with these details. Remember, large withholders don’t report PAYGWH on their activity statement, but they should still match up their reported STP and paid amounts.

If the ATO changes your PAYGWH cycle, update your payroll software to meet the new deadlines.

If you think your PAYGWH for the next financial year will be below the thresholds mentioned above, you can ask to stay on your current PAYGWH cycle. You must do this within 14 days after getting the ATO’s letter about the cycle change. Complete this form and send it to the ATO (or your tax agent can help).

As part of the economic stimulus triggered by the Corona Virus pandemic, the Federal Government has introduced the “Boosting Cash flow for Employers” measure or as we like to call it, the PAYGW Boost Credit. This measure promises to “refund” the PAYG withholding reported on the BAS or IAS by employers back into their integrated client accounts (ICA) as an offset against any existing BAS/IAS debt. To be clear, this is not a supply of cash to employers into their banks. This is simply crediting PAYGW back into the ICA to effectively reduce BAS/IAS debt. The only time an employer will see any cash is when a refund is created because the PAYGW credit is more than the whole activity statement debt. So who gets these payments, how much do they get and how do they get it? Read on to find out!

WHO IS ELIGIBLE?

Businesses will be eligible for this stimulus measure if they:

Held an ABN on 12 March 2020 and continue to be active

Are a small or medium business including NFP, sole trader, partnership, company and trust entities.

Have an aggregated turnover under $50M

Have made payments from which they have been required to withhold (even if this a zero amount). Such payments may include salary and wages, director’s fees, eligible termination payments, compensation payments and withholding from contractor fees.

Have made GST taxable, GST free or input taxed sales in a previous tax period since 1 July 2018 and lodged a relevant BAS on or before 12 March 2020.

HOW MUCH IS PAID?

PAYG withholding amounts will be credited back to the integrated client account (ICA) of between $20K and $50K. These credits are not income and as such will not be taxed. The do not have to be repaid ever. The good thing is that the PAYG withholding you report on your BAS will still be tax deductible. Note, if you have a tax debt on your ICA, the credit boost amount will simply pay down that debt.

HOW IS IT PAID?

These credits will be applied in two stages to integrated client accounts after 28th April 2020 and after the March 2020 quarter or monthly BAS is lodged. You do not have to apply for this measure, AND you do not receive any actual cash – this is credit only, not cash paid to your bank. The second stage credit will be applied in quarter 1 of 2020-21.

HOW DO THE PAYMENTS WORK?

Put simply, there are 2 payment stages for this measure. The first stage is a payment of up to $50K based on the amount of PAYGW reported on the March 2020 BAS. Examples below:

Quarterly Lodgers

If your March 2020 BAS shows a PAYGW amount of $12,000, this amount will be credited back to your ICA. In your June 2020 BAS, if a $14,000 PAYGW is reported, then this will also be sent back to the ICA. So far, a total of $26,000 has been credited. This is the first stage amount. The second stage amount will be the same as the first one i.e. $26,000 and will be credited to your ICA split evenly across June to September 2020.

Monthly Lodgers

If your March 2020 BAS shows a PAYGW amount of $12,000, this amount is multiplied by 3 (to take up amounts for January and February 2020) to give you a credit of $36,000. April, May and June 2020 BAS’s will continue to be lodged which may or may not total more than $50K. For this example, let’s say April was $10,000, May was $8,000 and June was $6,000. This will be a total PAYGW of $60,000. As the first stage payable can be no more than $50K, then $50K is all that will be credited to your ICA. The second stage payment will also be $50K.

What if my PAYGW is less than $10K or zero in my March 2020 BAS?

In this case, you will be credited $10K in the first stage of credits and another $10K in the second stage for a total of $20K.

The Government are starting to push through some rather drastic measures in regards to how small business reports to the Australian Tax Office (ATO). In my last blog, I wrote about one of those new measures, Simpler BAS – a new way to report GST for SME’s. In today’s blog, I will introduce another new reporting method called “Single Touch Payroll” (STP). As the name suggests, STP will affect business owners who are also employers. Read on to find out some facts if this affects you.

One of the questions I get from clients frequently is: what’s the difference between PAYG withholding & PAYG Income Tax Instalments? This is especially confusing for business owners who have never paid these taxes before and are new to the PAYG system. So what are these two taxes about and how do they affect your business?

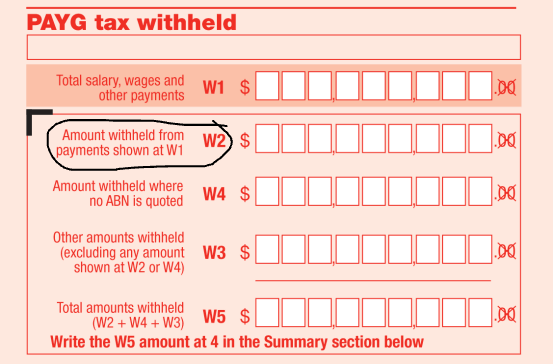

Welcome to part 2 of my 3-part blog about Business Activity Statement (BAS) labels. In part 1, I covered the “G” labels which are all used to report Goods and Services activities for GST registered businesses. In today’s blog, I will look at pay as you go income tax instalment (PAYG ITI) labels and pay as you go withholding (PAYG WH) labels.

Are you a new employer? Do you need help with getting started? Do you know what your employer obligations involve? Being an employer is a huge responsibility and brings with it added compliance to which you must adhere if you want to get it right. To assist you in this task, we have created the “Employers’ Toolbox”, a simple guide to getting started including all of the resources you will need along the way.

BAS Agents are now a very important part of the tax compliance landscape. They have been floating around since 2010 when the first group of agents became registered with the Tax Practitioners Board (TPB) after the passing down of TASA 2009. TASA 2009 is legislation that makes it illegal for anyone to charge a fee for providing tax and BAS Services without first being registered. Unfortunately, who BAS Agents are and what they do, has not been widely publicised by the TPB and as a result, many business owners have either never heard of them or certainly aren’t aware of what they do. Today’s blog, therefore, is about educating business owners about what BAS Agents can do for them in terms of their tax compliance and other related tasks. To this end, I have created a list of 20 tasks BAS Agents can do for business owners, of which perhaps they may not be aware. See below:

Are you a new employer? Do you need help with getting started? Do you know what your employer obligations involve? Being an employer is a huge responsibility and brings with it added compliance to which you must adhere if you want to get it right. To assist you in this task, we have created the “Employers’ Toolbox”, a simple guide to getting started including all of the resources you will need along the way.