Many businesses engage the services of professional bookkeepers, either as contractors or employees. These workers are involved in various aspects of a business’ operations, including sales, purchases, bank reconciliation, payroll and much more. But did you know that some services a bookkeeper provides are known as “BAS services” and some are basic bookkeeping services? There is a difference! In short, basic bookkeeping tasks and BAS services are not the same thing. Why is this important and why should business owners understand this concept? Read on to find out and to obtain a free bonus list of BAS services for your future reference.

Difference between bookkeeping and BAS services (and why it matters)

The Tax Practitioners Board (TPB) has a clear distinction between basic bookkeeping tasks and BAS services. They’ve made this distinction for a crucial reason: to ensure that only registered BAS agents perform BAS services for a fee. If an unregistered bookkeeper provides these services, they’re breaking the law.

This rule applies to external contractors. If you hire a bookkeeper as a contractor, it’s your responsibility as the business owner to ensure they are a registered BAS agent if you need them to perform BAS services. Conversely, if you have an employee bookkeeper, the TPB’s rules don’t apply, as the business owner is responsible for the accuracy of their work.

It’s a common misconception that all bookkeepers can handle all accounting tasks. Unregistered bookkeepers can only provide very basic services. Asking them to process payroll, for example, is technically illegal, as payroll is considered a BAS service. Let’s take a closer look at the differences.

What’s Considered a Basic Bookkeeping Task?

According to the TPB, an unregistered contractor can only provide basic bookkeeping services. These are generally the day-to-day tasks that help a business maintain its financial records. Examples include:

Bank reconciliations and data entry into an accounting system.

Processing payments.

Record keeping.

Collating and printing reports, such as draft Profit and Loss statements.

Coding transactions to accounts based on instructions from the client.

What’s Considered a BAS Service?

A registered BAS agent, on the other hand, can provide a much wider range of services. The TPB has a detailed list, but some of the most common BAS services include:

Preparing and lodging BAS (Business Activity Statements) and IAS (Instalment Activity Statements).

Preparing and lodging payroll through Single Touch Payroll (STP).

Calculating and lodging superannuation guarantee contributions.

You can download the full list from the TPB below for future reference.

It’s very common for business owners to hire external bookkeepers, but it’s essential to check their credentials. If a bookkeeper is not a registered BAS agent, they are legally limited to providing only basic bookkeeping tasks. It is illegal for them to charge for and perform BAS services.

Hiring an unregistered bookkeeper to handle BAS services not only puts you and your business at risk but also means the person may not have the necessary qualifications or experience to perform those tasks correctly.

The takeaway is simple: if you only need basic record-keeping, a non-registered bookkeeper may be a good fit. However, if you need someone to handle payroll, BAS, or other more complex services, you must hire a registered BAS agent. Always verify who you’re engaging and what services they are legally allowed to provide.

Key Takeaways

BAS services and basic bookkeeping tasks differ significantly, with specific legal restrictions around who can perform BAS services.

Only registered BAS agents can legally provide BAS services, while unregistered bookkeepers are limited to basic tasks.

Basic bookkeeping tasks include bank reconciliations, data entry, processing payments, and record keeping.

Common BAS services include preparing and lodging BAS, payroll through STP, and calculating superannuation contributions.

Business owners must verify a bookkeeper’s registration to avoid legal risks and ensure the correct handling of financial tasks.

In this blog I will show you how to set up a fully serviced novated lease for a motor vehicle in Xero. Before I begin, I would like to make it clear that every novated lease arrangement is different, depending on the agreement made between the employee and the lease provider. If this “how to” does not seem to match up with your requirements, please seek further advice from your tax agent or the lease provider. I will not be providing advice to readers about their individual requirements for their novated lease set ups, so please don’t ask! Again, seek advice from your tax professional or the lease provider company if you need help.

What is a Novated Lease?

Before diving into the “how-to” of this blog, it’s important to understand what a novated lease is. A Novated lease itself is a type of vehicle financing arrangement involving an employee, their employer and a leasing provider. Essentially, an employee is able to purchase a vehicle AND receive tax concessions under a salary sacrifice arrangement, orchestrated through payroll. Simply put, “to novate” means “to move with,” and in the context of a novated lease, it signifies that the employee’s vehicle and lease agreement can move with them if they change employers.

How a Novated Lease Works

Basically, a novated lease occurs as per the below steps:

An employee chooses a vehicle to buy.

A Leasing Provider provides a lease agreement to the employee which sees the employer take over the rights and obligations under the lease via a “deed of novation”. It should be noted that the deed of novation includes a clause that transfers the lease obligations back to the employee on termination of the lease or when the employee ceases employment with the employer.

The employee and employer enter into a salary sacrifice agreement whereby deductions are taken from the employee’s pay to fund the lease.

The employer pays the leasing provider with the payroll deduction funds. This means the employer is not out of pocket, both from a cash flow and tax perspective.

What is a Fully Serviced Novated Lease?

In this scenario, another party is introduced – a salary packaging provider. This provider will send the employer a reconciliation report the compares the actual motor vehicle costs against the novated lease estimated costs. If there is any variance, an adjustment must be made to the employee’s pre-tax deduction and sometimes, an adjustment is also required to the post-tax deduction.

A fully serviced novated lease includes, not only the lease repayments, but also other vehicle expenses such as:

Insurance

Maintenance like servicing, repairs and parts

Registration

Fuel

Roadside Assistance

Tolls

Car washing

This type of novated lease operates in the same way as described above, however it has an extra component which is FBT. The post-tax deduction is known as an Employee FBT Contribution which attracts GST. The employer also claims the GST on the novated lease expenses. The pre-tax deduction is calculated as the novated lease expenses minus the post-tax deduction (GST exclusive).

How to Set up the Fully Serviced Novated Lease in Xero

This “how to” will be based on the following novated lease example:

Sonia works for ABC Industries and is paid $120,000 plus super per annum on a monthly pay cycle. She decides to purchase a vehicle costing $60,000 and asks her employer if she can salary sacrifice the purchase via a fully serviced novated lease. Sonia’s employer agrees with the request and asks Billy’s Novated Lease Services to assist with the facilitation of the lease. Once the lease is in place, Billy’s Novated Lease Services provides the following information to ABC Industries:

The novated lease will be for 5 years and based on the following estimated costs, the fixed monthly amount will be $2,017.08. See the details below:

ITEM

GST Exclusive

GST

TOTAL

Lease Payment

14,000

1,400

15,400

Fuel

3,000

300

3,300

Servicing & Repairs

2,000

200

2,200

Registration

900

0

900

Insurance

1000

85

1085

Roadside Assistance

500

50

550

Tolls

400

40

440

Car Wash and Vacuum

300

30

330

TotalEstimated Annual Costs

22,100

2,105

24,205

Monthly Novated Lease Amount

1,841.66

175.42

2,017.08

The fringe benefit figure and related pre and post tax figures are also provided to ABC Industries as below:

The following steps will need to be actioned in order to set up the above lease in Xero:

Step 1 – Add the following accounts to the Chart of Accounts

Novated Lease Clearing Account – liability account, current liability; – BAS Excluded tax code; set up a separate account for each affected employee.

Novated Lease Expenses – expense account – BAS Excluded tax code; put under payroll costs like wages or super etc.

Employee FBT Contributions – revenue account – GST on Income tax code; place under non-trading income type e.g. “Other Income”

Fringe Benefits Tax – needed if an FBT liability arises; expense account – BAS Excluded tax code; place under general overheads.

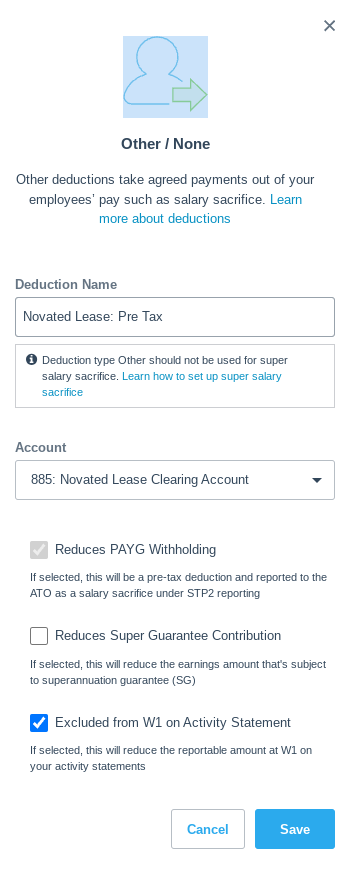

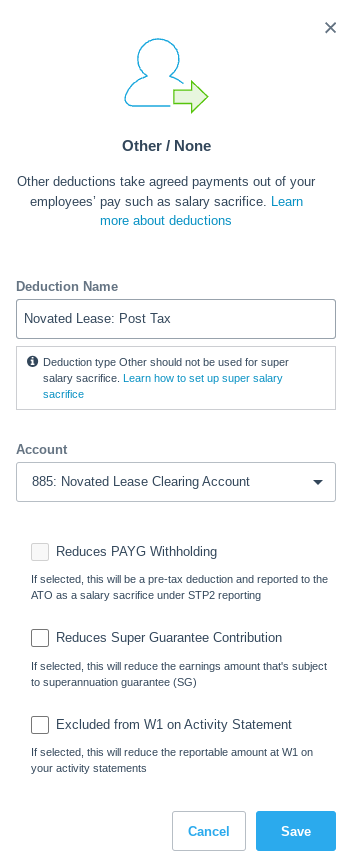

Step 2 – Set up the payroll tax deductions

Pre-Tax Novated Lease Deduction – reduces PAYG WH; may or may not reduce SG (but shouldn’t); excluded from W1; STP – Salary Sacrifice – Other Employee Benefits (type O); direct this deduction to the Novated Lease Clearing Account.

Post-Tax Novated Lease Deduction – Does not reduce PAYG WH; Does not reduce SG; Is not excluded from W1; STP – not reportable; direct this deduction to the Novated Lease Clearing Account.

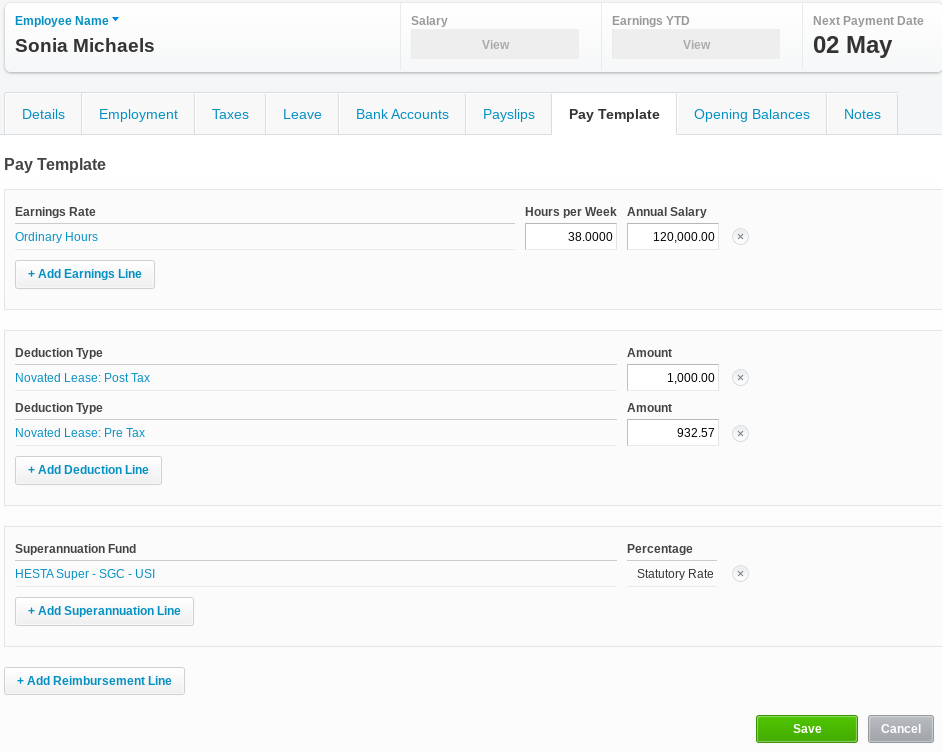

Step 3 – Set up the employee’s pay template & run a pay cycle

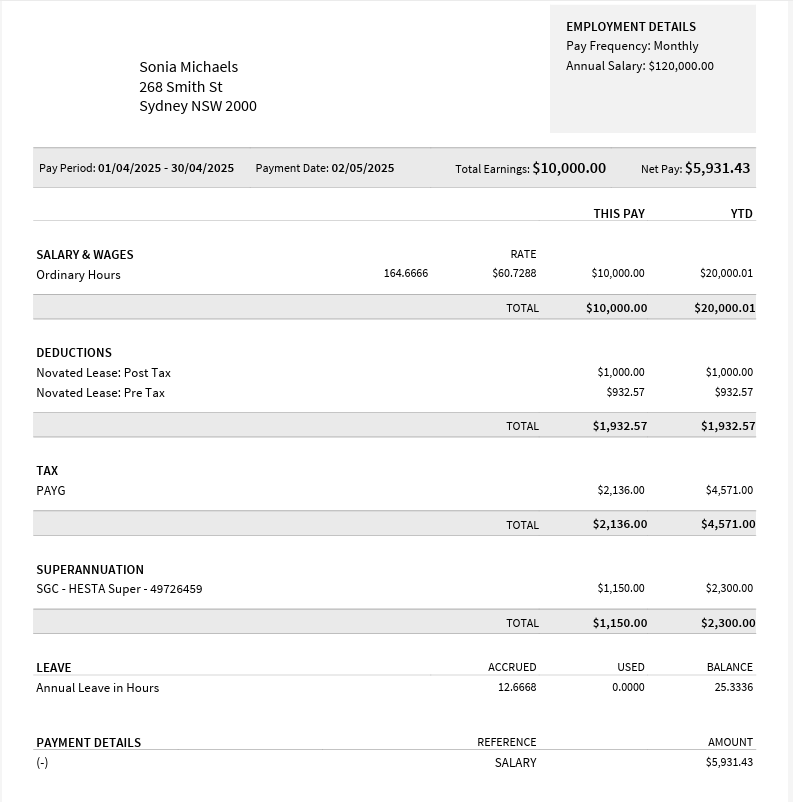

Open Sonia’s pay profile in Xero. Add the two deductions as above, then enter the figures provided by the lease provider. See below:

Now process the April pay run in Xero. Sonia’s payslip should look like the below example:

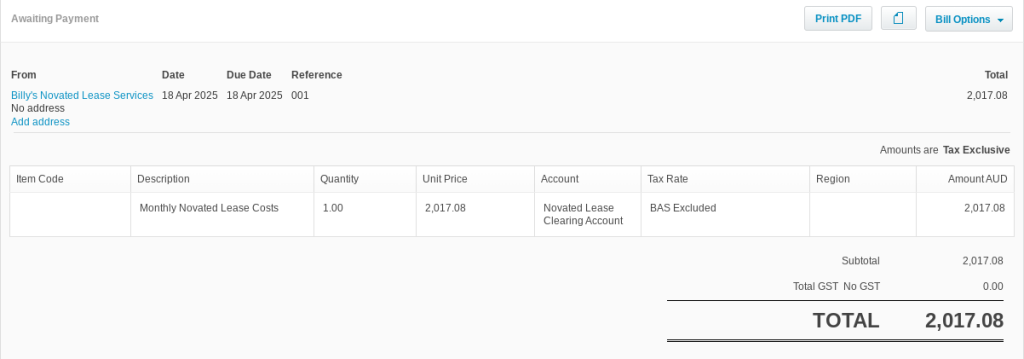

Step 4 – Record the lease provider’s invoice in Xero

In Xero, add the invoice received from the lease provider, “Billy’s Novated Lease Services”. Post the invoice to the Novated Lease Clearing Account with the BAS Excluded tax code. See an example below.

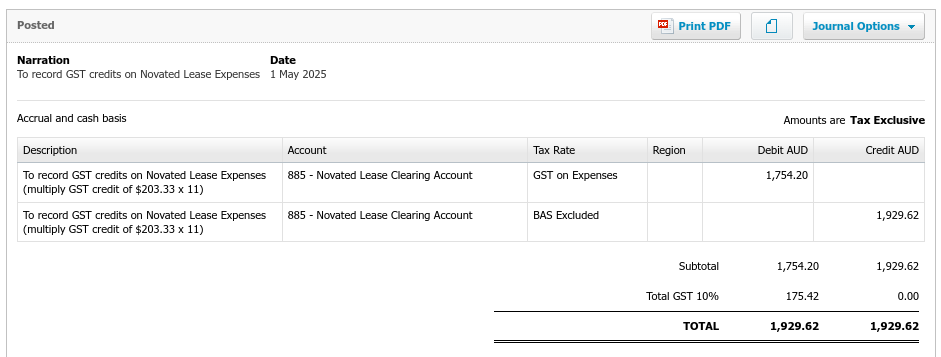

Step 5 – Record GST

There are two GST-related transactions to bring to account:

GST on the novated lease expenses

GST on the post-tax deduction

Each month, Billy’s Novated Lease Services will send ABC Industries a report detailing any GST credits available from the novated lease arrangement from the previous month. For ease of explaining this “how to”, we will assume the GST credits align with the example data. The GST credit therefore is $175.42. Now multiply the GST by 11. This will give rise to a figure of $1,929.62. To recognise the GST from the monthly report, enter the following journal:

Here, GST of $175.42 will move to the GST control account and become claimable in the BAS. The clearing account will receive net credit of $175.42.

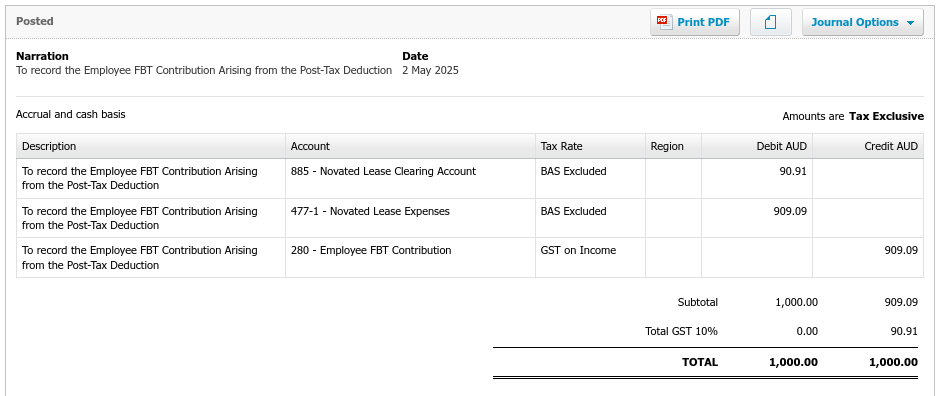

In order to take up the GST from the post-tax novated lease deduction i.e $90.91, enter the following journal:

The consequences of this journal will be:

$90.91 is credited to the GST control account;

The Novated Lease Clearing Account receives a debit of $90.91; and

Novated Lease Expenses receives a debit of $909.09.

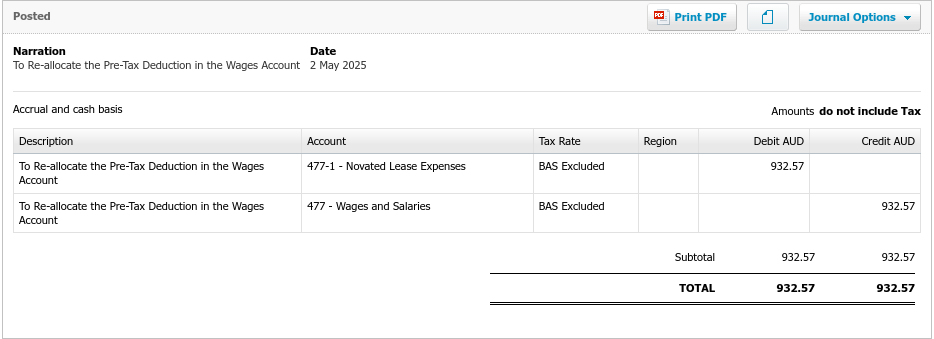

Step 6 – Correct overstated wages

The above payroll event has resulted in overstating the gross wages in the profit and loss. This is corrected by entering the following journal:

Behind the scenes – how are the accounts and the BAS affected by the novated lease?

Now that the above transactions have been processed in Xero, it would be prudent to show you how they affect the accounts and the BAS. Firstly, the novated lease clearing account has been cleared to zero as can be seen below. The account should return to zero each month after the payroll has been processed. If it doesn’t, you will need to investigate to find the cause!

The profit and loss shows the employee FBT contribution as other income and the lease and wage expenses are listed as expected:

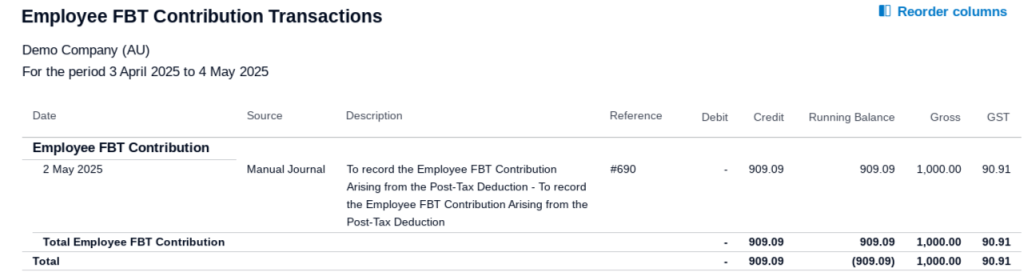

Now let’s drill into each profit and loss account to see the details. Looking at the FBT income I recorded at step 5, we can clearly see the GST posted of $90.91.

Next we can see the details behind the novated lease expenses recorded at step 5 and step 6. The total agrees with the monthly GST exclusive expense amount estimated by the lease provider.

Lastly, looking behind the wages expense transactions, we can clearly see how the wages are reduced by the reallocation of the pre-tax deduction:

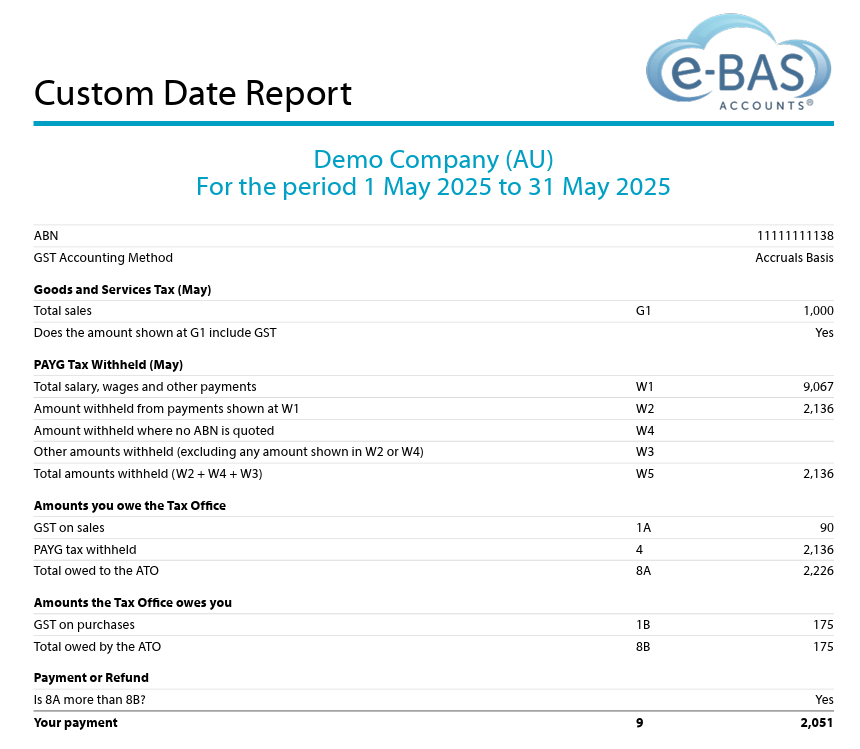

Now we will take a look at the BAS. Note the GST on sales of $90 from the FBT contribution and the GST on Purchases of $175 from the novated lease expenses journal. Also note the reduced gross wages figure which is the correct figure to report to the ATO.

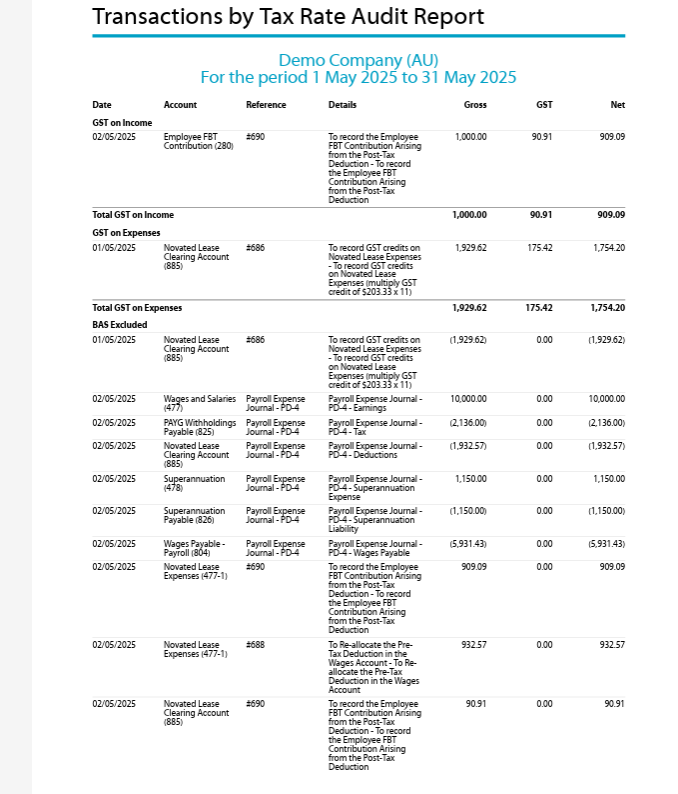

Drilling down into each GST type below, shows us the origin of the figures:

Summary

Setting up a fully serviced novated lease in Xero, as outlined in this guide, offers one approach to managing these arrangements. It’s important to remember that variations in novated lease structures exist, each with its own implications for employee wages and payroll processing. While the data you receive from your lease provider might differ from the steps detailed here, this ‘how-to’ should provide a solid foundation for establishing the necessary accounts and configuring tax deductions within Xero. Please note that I cannot offer guidance on your specific lease agreement, however, I’m happy to address any questions you have about the instructions provided in this blog. Finally, the example figures used in this guide are purely illustrative and should not be evaluated for their financial accuracy or feasibility. The primary goal here is to demonstrate the mechanics of setting up a novated lease within Xero, so please focus on the procedural steps rather than the example’s specific details.

In a previous blog, I discussed the challenges agents and clients face because of Client Agent Linking (CAL). Many of the issues encountered are related to setting up various digital identity software and/or not understanding the CAL process. In this blog, I will share useful links, videos and phone numbers to help those stumbling through this difficult task!

As mentioned, the CAL process is complicated. It involves setting up a myGovID, linking the ABN to the myGovID in Relationship Authorisation Manager (RAM), logging into Online Services for Business (OSB), nominating a new agent and finally advising the agent that the nomination has occurred. The links to assist with setting up myGovID, RAM and OSB are below, along with a step-by-step guide to CAL both in written and video format. Some phone numbers are listed for those who prefer to call a human being! I hope this helps those who are struggling with CAL.

CAL – Useful Links

How to nominate an agent in online services for business (download)

This is the fourth part in a series I’m calling “How-To”. The first part was about insurance bills, the second part was about VicRoads registration bills and the third part was about chattel mortgages. I will be using Xero for the example, but don’t worry if you use another software, the basic rules will still apply.

The fourth how-to is about how to account for hire purchases in your accounting software. A hire purchase arrangement is an agreement to purchase goods in instalments.

Step 1

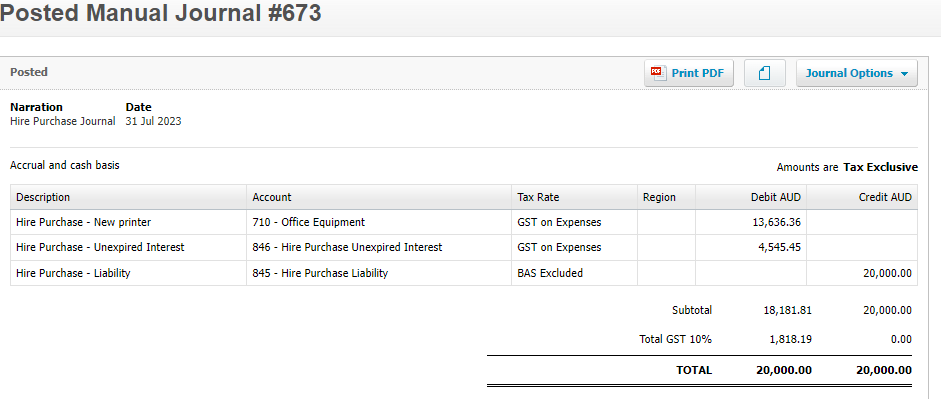

Let’s pretend that your business has purchased a new printer with all the bells and whistles for $15K via a hire purchase agreement, plus $5,000 interest. For this example, the hire purchase is for 30 months without a residual (balloon) payment at the end of the period. Note, that most hire purchase agreements will include a balloon component (check your documentation). The first thing to do is collect all of the documentation. You will need the hire purchase agreement, the invoice, and the interest amortisation schedule. The hire purchase company will provide all of this to you at the point of purchase. To begin the process, create some accounts in your accounting software:

Office Equipment (Asset GST Inc)

Hire Purchase Unexpired Interest (Liability GST Inc)

Hire Purchase Liability (Liability BAS Excluded)

Interest Expense – Hire Purchase (Expense BAS Excluded)

Note, For any Hire Purchase Agreement made after 1/7/2012, both the purchase price of the asset and all interest charges and fees are subject to GST. (see notes at the end of the blog)

Step 2

Now you can enter this journal which adds the purchase of the printer into the accounts:

Check your balance sheet. It should look like this:

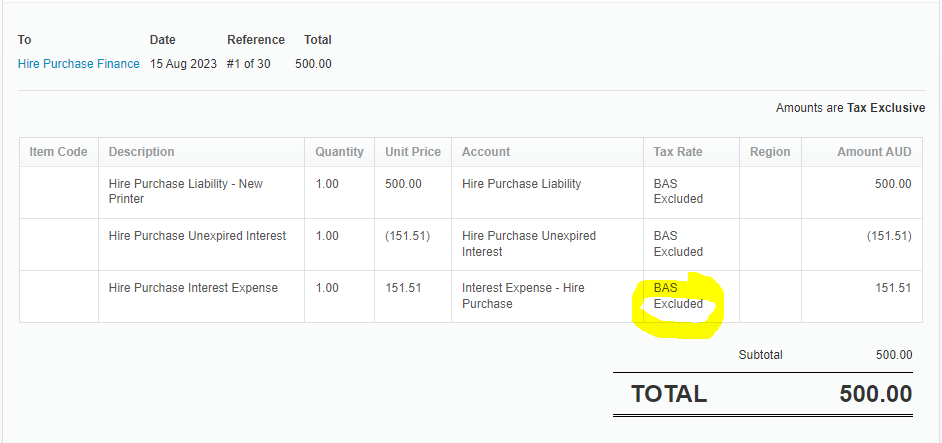

Step 3

When it comes time to record the first repayment to the finance company, your entry will look like this (assuming each repayment is $500 (30 x $500 = $15K)). Note, that the tax code for the interest expense account is BAS Excluded. This is because the GST on the interest component of the hire purchase was claimed when the purchase was entered initially (see journal). Therefore the monthly repayments of interest are not reportable on the BAS.

Step 4

Check that the balances in the balance sheet are reduced by the first repayment – see below. Note that I have evenly split the interest repayments into amounts of $151.51 for this example ($4,545.45 divided by 30 payments). However, you will need to enter the interest amounts as per your amortisation schedule and these won’t be exactly the figures divisible by the number of repayments. Something to keep in mind!

GST rules for hire purchases

For hire purchase agreements entered into on or after 1 July 2012, all components of the transaction are subject to GST including: • The upfront purchase price of the asset financed under the agreement • Interest charges, and • Any other associated fees.

This is the case regardless of whether you account on a cash or accrual basis.

This means that taxpayers on a cash accounting basis can claim the full amount of any available GST credit at the time the first payment is invoiced or paidunder the hire purchase.

This was the last part of our How-To series (for now). I hope you found this series useful. For further details about hire purchase agreements and GST, go to this ATO webpage.

This is the third part in a series I’m calling “How-To”. The first part was about entering insurance bills and the second part was about how to enter a VicRoads registration bill. I will be using Xero to present the example, but don’t worry if you use another software, the basic rules will still apply.

The third how-to is about how to enter a Chattel Mortgage asset and associated loan into your accounting software.

Step 1

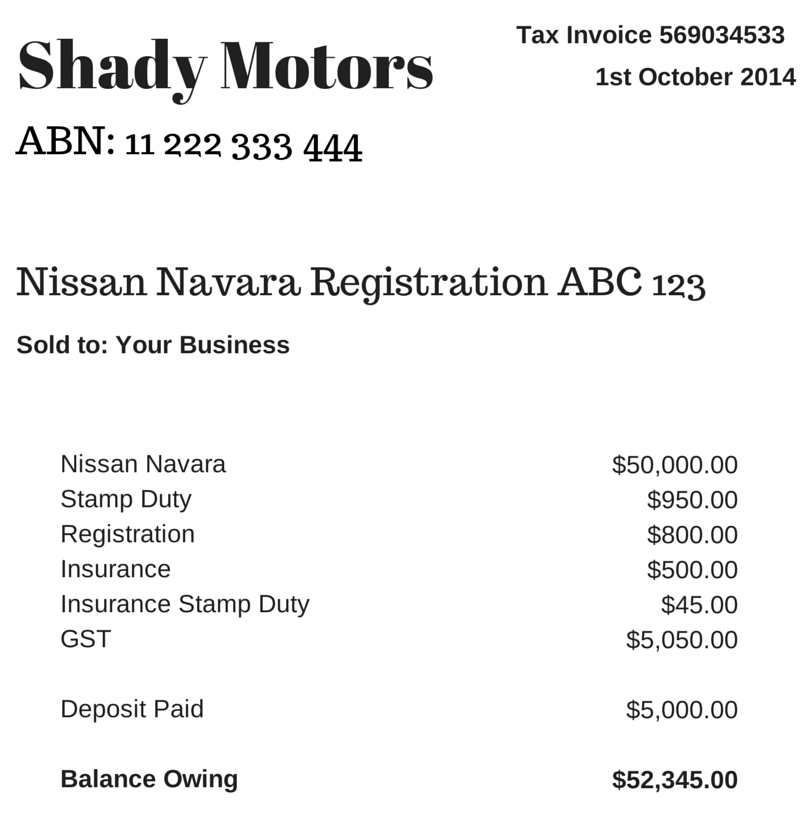

Let’s say your business has purchased a new motor vehicle. The invoice from the vehicle dealer might look something like the below example. Grab your invoice now.

Step 2

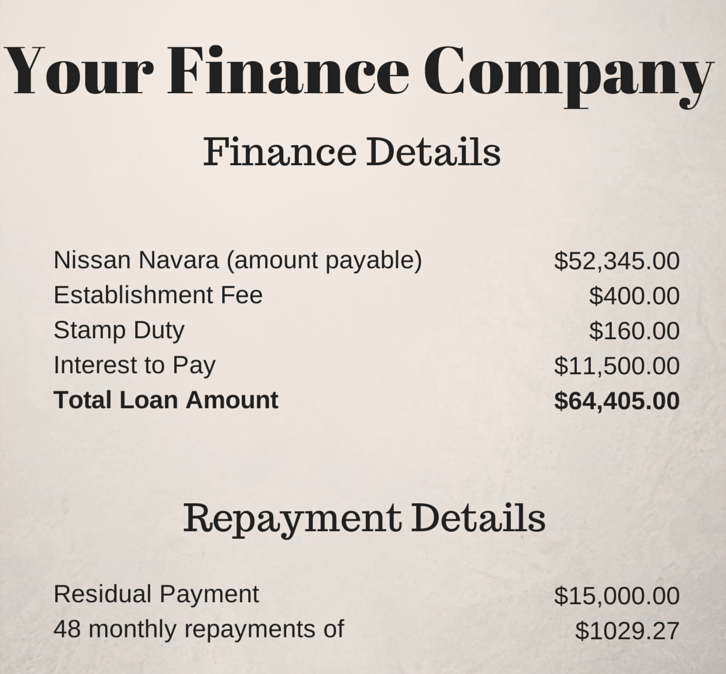

The finance company loan schedule is also required. It may look something like the below example. Grab you loan schedule now.

Step 3

Create the following accounts in your software (check first because some may already exist):

Deposit Paid (Current Asset) – no tax code

Motor Vehicles at Cost (Non-Current Asset) – apply capital expense including GST tax code

Chattel Mortgage (Motor Vehicle) (Non-Current Liability) – no tax code

Chattel Mortgage Interest Charges (Expense) – no tax code

Chattel Mortgage Fees & Charges – tax code varies, could be Free or GST inclusive (check your documentation)

Motor Vehicle Registration (Expense) – apply GST Free tax code

Motor Vehicle Insurance (Expense) – apply GST inclusive tax code

Unexpired Term Interest (Non-Current Liability) – no tax code

Step 4

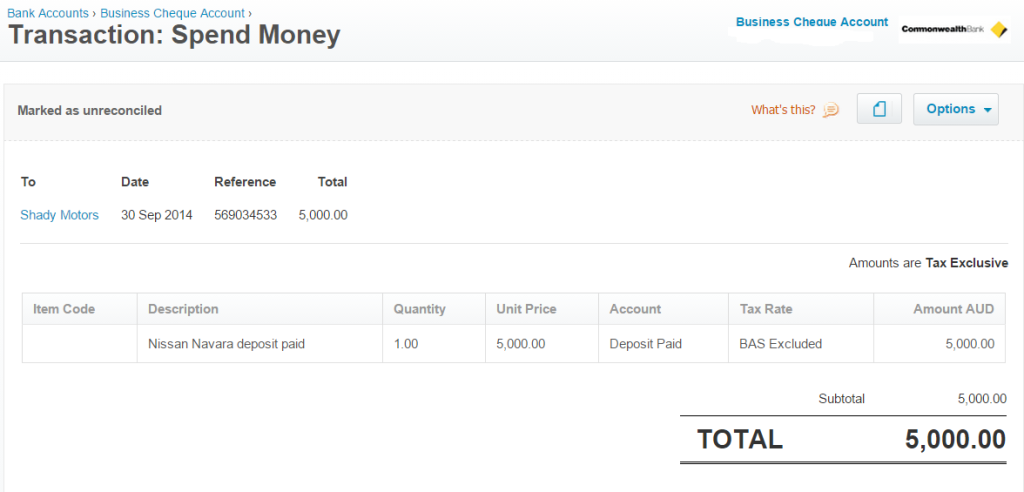

First enter a spend money transaction to record the payment of the deposit:

Step 5

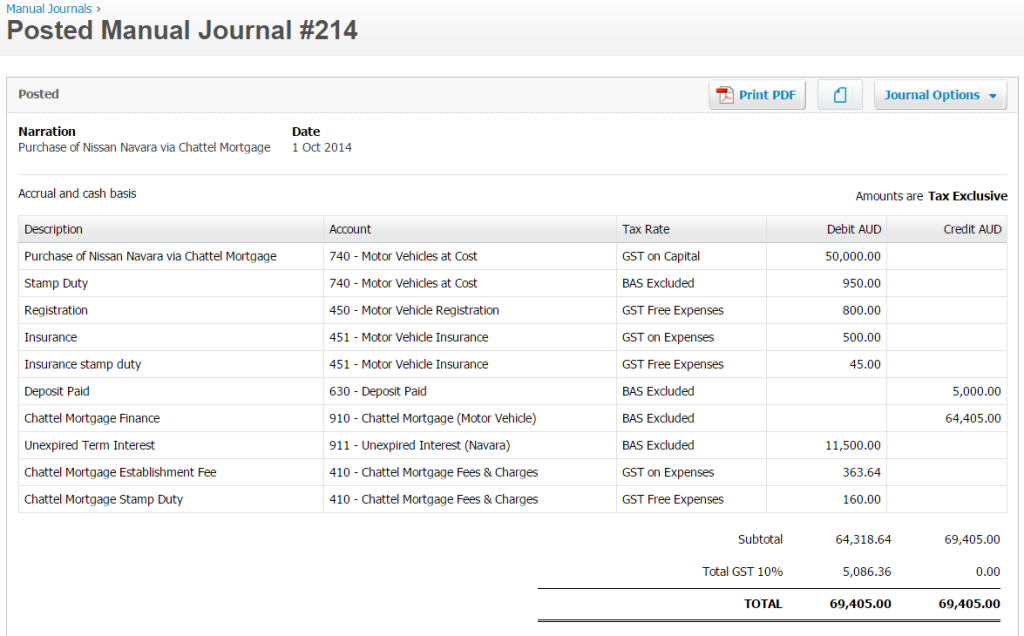

Next, enter this journal to record the purchase of the new vehicle:

Step 6

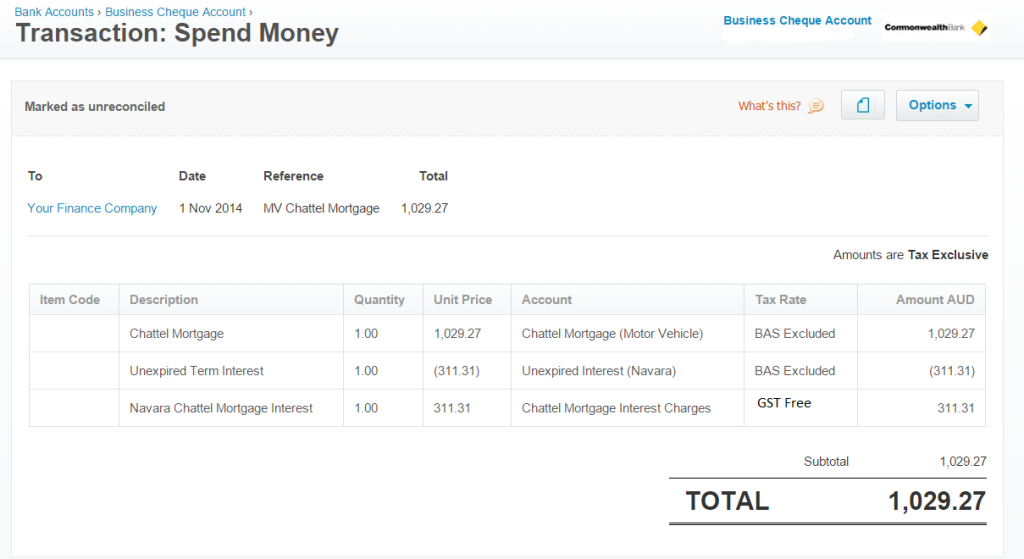

When it comes time to make a repayment to the finance company, enter a spend money transaction like this:

Bonus Tip!

Sometimes it isn’t possible to obtain the loan repayment schedule for whatever reason. When this happens, you need to create your own. I use this amortisation calculator by Bret Whissel. It has served me well over the years. I hope you find it useful too.

Last week, I started a bookkeeping resource series called “How To”. Each week I will share instructions with you about how to enter some common transactions. I will be using Xero to present the example, but don’t worry if you use another software, the basic rules will still apply. Last week I explained how to enter an insurance bill.

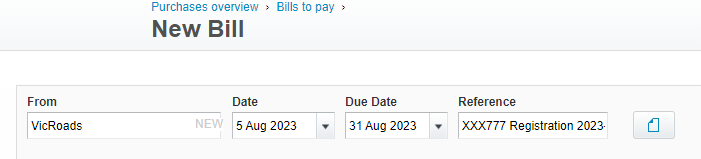

The second how-to is about how to enter a VicRoads registration expense/bill into your accounts.

Step 1

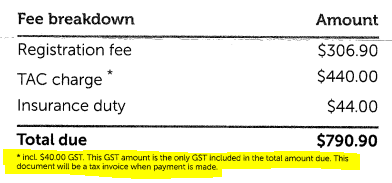

Grab your VicRoads bill and go to the part where it shows you the breakdown of charges. It may look something like this:

Step 2

Log into your software and go to the area where you enter bills.

Step 3

Enter the VicRoads as the supplier, the relevant dates and the reference number or name as below:

Step 4

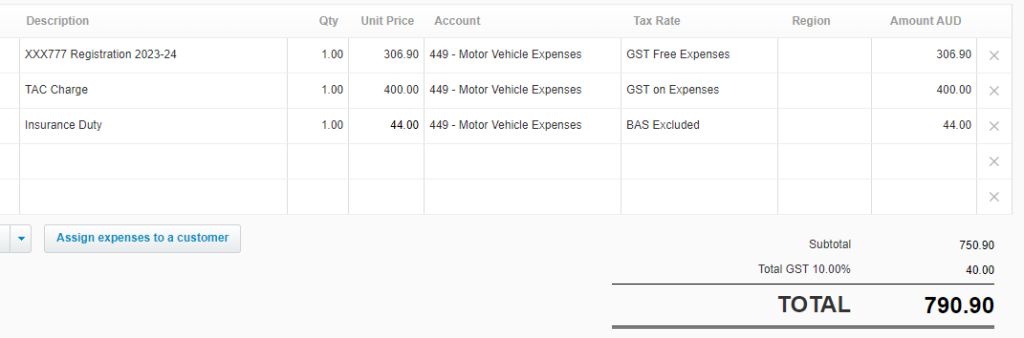

Enter a line in the bill for each charge shown on the bill. The registration fee is GST-free, the TAC charge includes GST and the insurance duty is BAS Excluded. If you are entitled to claim 100% of motor vehicle costs in your business, then you can claim the full GST amount on the TAC charge. Time and time again, I see clients entering the full amount of the registration expense as GST-free. While they are partly right, they are also missing out on claiming the GST of the TAC charge. Also, relevant here is the choice of account for expense coding – you may like a general account such as this one “Motor Vehicle Expenses”, or you may like to split your costs out in a more detailed manner and have an account for each type of car expense, in this case, “Motor Vehicle Registration”. It just depends on how much detail you want to see in your profit and loss report.

Step 5

Check that the GST amount agrees with the VicRoads bill. In this case, it is $40.00.

Step 6

Approve the bill to ensure the expense is added to the accounts correctly.

Final words…

So that’s it for this week’s “how-to”. I hope you learned something new. One thing I’d like to add about VicRoads “bills” before I close off this blog, is that to obtain an actual bill, you do have to have an account with VicRoads. They used to send out the document in the mail, but not anymore – it’s all online, like everything these days. Here’s the link to VicRoads where you can make an account if you haven’t already done so.

Bonus Tip!

For any bookkeepers out there who know the pain of not ever receiving an actual VicRoads bill from clients (who probably don’t know how to get it – see notes above), which makes data entry nearly impossible, here is the link to the TAC registration rates for FY24. This document provides the breakdown of TAC and insurance duty fees based on postcode and vehicle type. An excellent resource that I am sure you will use time and time again. There is also an online calculator you can use on the VicRoads website that will provide the figures you need easily. Here is the link for the calculator. Either resource will get you the information you need. You’re welcome by the way!

This week, I am starting a bookkeeping resource series called “How To” (not very original, I know!). Each week I will share instructions with you about how to enter some common transactions. I will be using Xero to present the example, but don’t worry if you use another software, the basic rules will still apply.

So here goes, the first how-to is about how to enter an insurance bill into your accounts the right way.

Step 1

Grab your insurance bill and go to the part where it shows you the breakdown of charges. It may look something like this:

Step 2

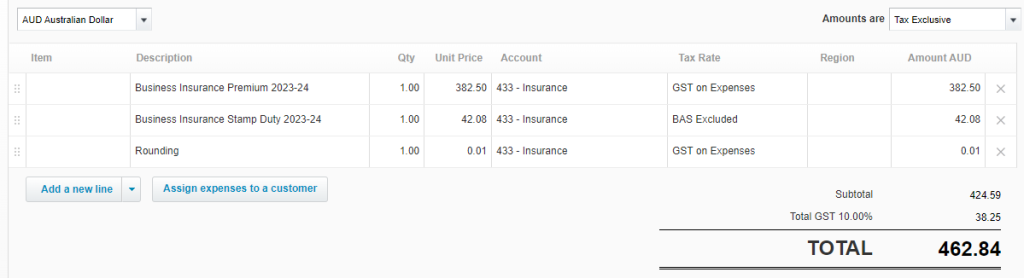

Enter a line in the bill for each charge shown on the bill. In this case, there is one for the premium and one for the stamp duty component. Select the insurance account you want to use – you may have one for business insurance and another for motor vehicle insurance etc. Notice that the premium figure is plus GST, whereas the stamp duty is BAS excluded. This is because stamp duty does not attract GST. It is very important to break up your insurance bill like this and to never enter a bill 100% inclusive of GST. Doing so will mean that you overclaim GST in your BAS.

Step 3

Check that the GST amount agrees with the insurance bill. In this case, it is $38.25 which is one cent less than our bill, hence the rounding line I have added to agree the total amount with the supplier’s bill.

Step 4

Approve the bill to ensure the expense is added to the accounts correctly.

Final Words…

So that’s it for this week’s “how-to”. I hope you learned something new. Please note that this insurance example is pretty basic. Some insurance bills have extra charges which may or may not include GST. The trick to getting these sorts of more complex bills entered correctly is to ensure the GST figure in the bill agrees with your software entry. If it doesn’t, you need to check each charge for its GST status i.e. some items will include GST and others may be GST-free or GST-exempt.

Over the last couple of years, I’ve moved away from written content to podcasts as my preferred choice of learning and research. Podcasts are great because you can listen to them at any time, doing anything, and privately, too, if you use earphones or earbuds. I usually walk daily and listen to a podcast at the same time – getting my exercise and racking up CPE points simultaneously – win-win!

I have many interests and there are podcasts for just about any topic you can imagine. Being a bookkeeper, I have found several podcasts about tax and bookkeeping, and over the years, have narrowed the list down to three podcasts that resonate with me the most. Here is my list:

Two Drunk Accountants: This podcast is hilarious! If you thought that accounting and tax topics could never be interesting or even funny, you are in for a big surprise! Tim Garth and Dan Osborne of CATS Accountants are the voices behind this thoroughly entertaining podcast. I find that I am laughing from beginning to end but am being educated at the same time. I enjoy this podcast and you will too! Here is the link to hear the boys bang on about their industry and their lives in general.

ICB News Channel: The Institute of Certified Bookkeepers has a podcast that is published monthly, based on topics from their newsletter. Rob Marshall, the Support and Resource Manager at ICB, runs the podcast which often includes interviews with current stakeholders involved in the bookkeeping industry. If you want to keep up with the changing face of bookkeeping and also top up your CPE points, this podcast is the one to choose. Find this podcast here.

Tax InVoice: This podcast is delivered by the ATO. Certainly not as entertaining as the Two Drunk Accountants (because let’s face it, “Two Drunk ATO Tax Specialists” doesn’t have the same ring!), the podcast will dot the i’s and cross the t’s so far as covering many tax issues and topics. Covering everything from working from home to crypto assets, Tax InVoice is a purely tax-based podcast but I find it is an easier platform to use to try and understand tax topics which can be difficult to do via written text only. You can find the 50-plus episodes of Tax InVoice here.

I’m sure if you search, you’ll find many other bookkeeping/tax podcasts. As I said earlier, I did follow about 6 or 7 back in the day but have slowly removed the ones that I didn’t find useful or enjoy. There aren’t too many Australian tax podcasts really, so if you do a search, you’ll probably find several American-based ones. These ones have their place, but if you’re after Australian tax information, you need to ensure you choose Australian podcasts. I hope you find this information useful and if you haven’t delved into the world of podcasts yet, perhaps you can start with one or two from my list.

Do you listen to a bookkeeping podcast that you think is great? Why not share it with other readers in the comments section below?

Unless you’ve been living under a rock, you would undoubtedly have heard the term artificial intelligence or “AI”. AI is the new buzzword and seems to be everywhere you look. In particular, most accounting software, and many other apps have embraced AI and have made it a part of their interface.

While some may be dubious about AI (even afraid), the fact is, that it is here to stay and has been a part of the way we use technology for a long time. Google apps including Gmail and GDrive, apps like “Grammarly” and other apps that make suggestions as you type, for example, are all using AI to enhance the user experience and basically make life easier.

Given AI is already here and we use it daily (even though we may not be aware of it), I have started to wonder how bookkeepers can use it to assist with daily tasks. To that end, I have done some research into how we can use ChatGPT for this purpose.

What is ChatGPT?

ChatGPT stands for Chat Generative Pre-training Transformer. It was launched in November 2022 and is a remarkable text-based chatbot. It enables users to effortlessly type queries and receive accurate answers, as well as efficiently complete tedious tasks. This advanced chatbot is trained with extensive data, allowing it to generate responses that closely resemble human-like interactions. You can download the ChatGPT apps from your favourite app store.

So now that we know what it is, how can bookkeepers use ChatGPT? There are actually many ways to use it, but here are 10 ideas to get you started.

Writing those “difficult” emails to clients. Sometimes as bookkeepers, we need to tell our clients they have to go, or we are putting our prices up or we found something dodgy in their accounts, etc. Ask ChatGPT to write the email for you by telling it what the email is about. You will receive a professionally written email script in seconds.

Creating Excel formulas. Tell ChatGPT what you want to calculate in a cell or column and provide the data to work with and it will create the formula for you.Here is an example of how this might work.

Creating journal entries. ChatGPT can extract information from receipts, such as dates, seller names, and amounts. Just provide the dataset, and ChatGPT will analyze it and input the client information for you. More specifically, the prompt you would use would be: “Use the following transaction details (add transaction text) and amount to create a journal using these account names (Add accounts) using (Add accounting system)”

Creating checklists and subtasks. Ask ChatGPT to create a list of steps to complete any bookkeeping process. The result can be modified to suit your needs and business. You can also ask it to create subtasks for each of the steps inside a checklist.

Creating client questionnaires. Ask ChatGPT to suggest a list of questions to ask new clients during client onboarding.

Creating client onboarding checklists. Ask ChatGPT to create a checklist for you when onboarding a new client. You can tell it some basic details like number of employees and business structure.

Creating an engagement letter. Ask ChatGPT what to include in an engagement letter for a client with XYZ requirements. Adjust to suit your business requirements.

Staff onboarding checklist and letters of offer. Ask it to create a checklist for onboarding staff either for your business or for a client. Also, ask it to create letters of offer based on the details you provide. Adjust to suit your business.

Creating email templates. Make a list of the type of emails you write continuously e.g. a request for information. Ask ChatGPT to write these emails for you. Update the details to suit your business and then save them as templates.

Creating copy for your blog or website. Tell ChatGPT what you want to write about e.g. ideas for your About Page. Ask it to write you the copy for this page. You can do the same thing for your blogs. Simply provide it with some basic information e.g. how GST applies to food sales in Australia, and ask it to provide you with copy for your blog. Of course, you should check the details it delivers for accuracy and currency before publishing.

I hope these ideas, or “prompts” as they are known, give you the motivation to start to play around with ChatGPT in your bookkeeping business. Obviously, the sky is the limit regarding what you can do with ChatGPT. I’m sure once you get started, you will discover many more ways to use it in your business. If you would like to share any prompts you currently use with ChatGPT, please add them below in the comments. I’m sure other bookkeepers would love the extra motivation!

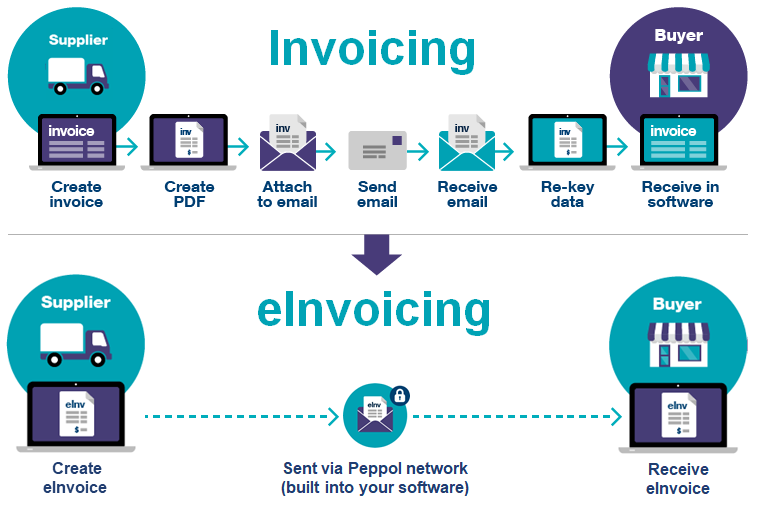

eInvoicing is a new way to securely send and receive invoices between businesses via a secure global public network known as Peppol. The Australian Peppol Authority is the ATO. eInvoicing, despite being a popular and efficient method of transacting, is not mandatory.

A buyer and a supplier must both be registered with Peppol in order to use eInvoicing. This is done via your accounting software (if it offers eInvoicing functionality). Larger businesses may need to use alternative options in order to connect to the network.

Why eInvoicing?

eInvoicing is secure and time-efficient. It removes the need for using email or snail mail as methods of sending invoices and therefore, is more secure. It also removes the need to key in invoice data when an invoice is received and/or scan and attach PDF copies of the invoice. Data entry error is also heavily reduced when using eInvoicing due to little or no keying in of details required. When an invoice is received via eInvoicing, you would simply go through your normal approval process and then prepare to pay the invoice when ready. The below image is from the Institute of Certified Bookkeepers and explains the difference between the current invoicing process you probably use now, and the eInvoicing process which is much simpler.

/

How do I know if my supplier or customer is eInvoicing-enabled?

When you or your supplier becomes eInvoice-enabled, you will be listed in the Peppol Directory. You can search the directory to see if your contact can receive or send eInvoices.

How do I know if my software product is eInvoicing-ready?

All software products that offer eInvoicing functionality are listed in this register on the ATO website. Some products are accounting packages and some offer online web portals for eInvoicing.

Below are 3 of the most popular online accounting packages which are eInvoicing-ready now. Each software link below will assist you to get started using eInvoicing and explain the process specific to that software. It’s important to note that MYOB and Xero do not charge anything extra to use eInvoicing which is excellent! Reckon has monthly packages including eInvoicing.

Not ready to commit to eInvoicing? Need more information?

eInvoicing is relatively new, although large companies and government departments have been using it for quite some time now. Small businesses are slowly engaging in this new method, with the uptake increasing continually. It is understandable that you may not be ready to make the jump to eInvoicing or even require it at this stage in your business development. If you would like to do some further research before moving forward, here are some useful links: