If your business has outstanding invoices, and let’s face it, most businesses have them, your cash flow is probably suffering. This isn’t great when you have to pay rent, payroll and suppliers etc. Enter FundTap.

FundTap, is a fintech innovator transforming invoice financing. They offer a flexible way to access funds tied up in unpaid invoices, empowering businesses without traditional lending hurdles.

Unlock Your Working Capital, On Your Terms

FundTap provides short-term funding solutions tailored to your needs, whether for a single $1,000 invoice or multiple invoices up to $150,000. Their pay-as-you-go model removes ongoing repayments or lengthy contracts, giving you control over your finances.

Speed and Simplicity at Your Fingertips

Skip lengthy applications and paperwork. FundTap’s online application and integration with platforms like Xero, QuickBooks Online, MYOB, and Reckon allow you to receive funds in hours. This will assist you to cover urgent expenses and improve your cash flow.

As Claire Reuss, Relationship Manager at FundTap, notes, “Getting finance as a small business is often a struggle. Many SMEs wait 60 to 75 days for payments while needing to cover rent, payroll, and supplies. FundTap solves this by giving quick access to funds tied up in unpaid invoices.”

Flexibility That Fits Your Business

FundTap stands out with:

No establishment fees: Saving you money.

No contracts: Use services only when needed.

No minimum funding requirements: Even small invoices unlock capital.

This inclusivity benefits businesses of all sizes across various industries.

Effortless Repayment: Automation at its Best

Because FundTap is connected to your accounting file, it can detect when your customers have paid invoices. FundTap will then initiate direct debit for the advanced amount plus a small fee. This integration saves time and ensures efficient repayment. If payments are late, FundTap adjusts the debit date. Early repayment incurs no extra fees.

Getting Started is Simple:

FundTap’s setup process:

Firstly, FundTap will ask you to answer some questions to ascertain your eligibility for funding – see below:

Does your business operate in Australia or NZ?

Do you invoice for services/goods?

How long have you been operating? (0-3 months, 3-12 months, 12+ months)

What is your average monthly turnover? (Under $5,000, $5,000 – $50,000, $50,000 – $500,000, $500,000+)

If your business is eligible, then all you have to do is follow these simple steps to get set up:

Connect your software: Connect FundTap to Xero, QBO, MYOB or Reckon.

Select the invoice/s to fund

Receive funds within hours from FundTap

Automated repayment: FundTap will direct debit your account once your customer pays you.

Take Control of Your Cash Flow Today

Don’t let unpaid invoices hold you back. FundTap offers a modern, flexible way to access working capital, allowing you to focus on growing your business.

Disclaimer

This post is shared with our blog readers for their benefit only. The information provided has come from the Australian Bookkeepers Association, of which I am a member. e-BAS Accounts is not affiliated with FundTap and does not receive commissions from FundTap for this post.

In that last couple of weeks, I have had 2 new clients ask me if they need to register for GST. Given that the answer is not entirely straightforward, I thought I would share the answer I gave these clients with my blog readers as it could help another business owner who may be considering the same thing.

Registering for GST is dependent on some variables. These are listed below:

Compulsory GST Registration

You or your business must register for GST if any of the following apply:

Claiming Fuel Tax Credits (required, regardless of turnover)

Providing taxi/limousine services (required, including ride-sharing)

Exceeding the turnover threshold: (required if your projected or current GST turnover is $75,000 or more ($150,000 for non-profits)). “Turnover” is your business income, excluding certain things like GST and sales to associates. If a business exceeds the turnover, it must register within 21 days or face paying GST retroactively, plus penalties. Note, to determine your current GST turnover, look at your turnover for the current month plus the previous 11 months. To determine your projected turnover, look at the current month plus the next 11 months.

Voluntary GST Registration

If you don’t have to register, should you? Consider these pros and cons for your business:

Pros

Claiming back GST on business expenses.

Increased business credibility – being registered could make your business look more professional.

Some suppliers prefer to deal with GST-registered businesses.

If you are an exporter/importer, being GST-registered can make things easier.

Cons

More paperwork and administration.

Potentially extra costs if you choose to use an external tax professional to prepare and lodge your business activity statements (BAS).

Prices might seem higher to non-GST registered customers so they may avoid buying from you.

Cash flow can be tricky, especially when it comes to setting aside the GST collected from sales. It’s crucial to resist the temptation to use those funds before your BAS is due.

GST-registered businesses may be at increased risk for ATO audits.

Key takeaway: GST registration is mandatory in certain situations. If it’s optional, weigh the pros and cons carefully based on your business needs. If a business does choose to register, generally it must stay registered for at least 12 months.

How to register for GST

If you decide to register for GST or are required to do so, you can do this when you apply for an ABN (Australian Business Number). Note, you must have an ABN before you can apply for GST registration. To set this up go the Australian Business Register website.

If your business is up and running and you want to add GST registration to your ABN, go to the Business Registration Register, or Online Services for Business (OSFB). Alternatively, you can ask your tax professional to register your business for GST on your behalf.

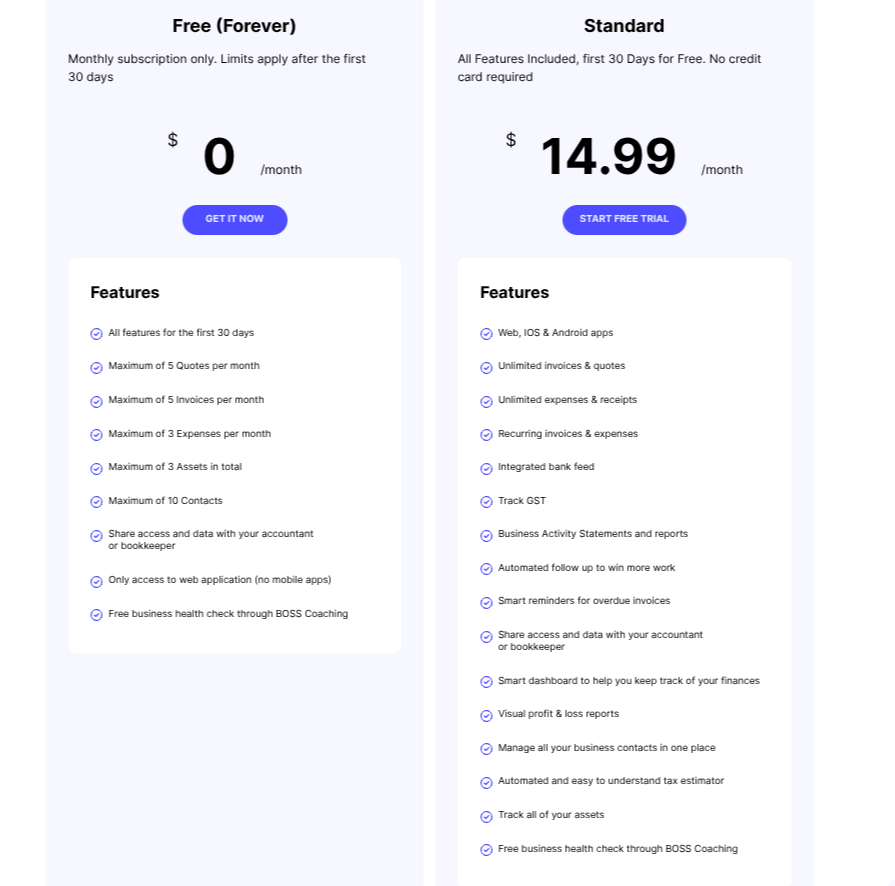

Recently, I have seen some new software players in the accounting software space. These developers have created software just for sole traders, freelancers and the self-employed. I think this is a great idea as some accounting software can be very overwhelming and complicated and contain many functions that sole operators just don’t require. This week I am reviewing 2 of these new software: Solo by MYOB and Sole.

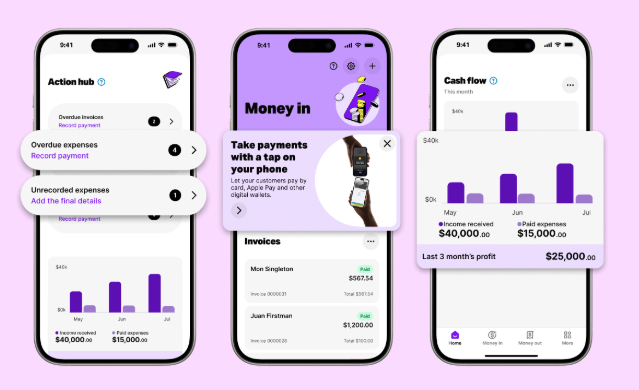

Sole is an Australian accounting software that offers GST tracking, expense categorisation, invoicing, quotes, bank feeds customer reminders, tax reporting tools and financial reporting. There is both a web and mobile app. The user can invite their tax professional to connect to the file if required. The cost is reasonable as can be seen below. There is also a free forever option, however the features are somewhat limited. Sole does not offer payroll but has partnered with Clockon to assist with Single Touch Payroll reporting. Sole is not suitable if your business has advanced inventory management needs, relies heavily on external CRM systems or requires integration with several other platforms.

Solo is an MYOB product which launched in November 2024. It is a mobile app only, that is, it isn’t available on the web. Solo does not include payroll or inventory management. At the time of writing this blog, users cannot invite their tax professionals into the Sole file, however, reports can be downloaded and provided to bookkeepers etc. Solo is an app available on IOS and Android and offers expense tracking, record-keeping, tax and GST tracking, invoicing and in-person “Tap to Pay” payments, income snapshot reports and bank feeds. MYOB reports that more features will become available during 2025. The current price for Solo is $12 for 12 months and then $99 per year following the first year.

These two software tools could be very helpful for “solopreneurs”, especially startups. Any product that helps business owners get organized, manage record-keeping, and assist with reporting is valuable. While these tools are quite basic in functionality, they are a good starting point and help users understand bookkeeping and tax requirements. I believe these software tools will become very popular, and I’m sure more similar products will follow in their footsteps soon.

In our last blog, we covered whether or not a side hustle like selling items on eBay or being an influencer could be a business and how to tell when a side hustle turns from being hobby-like activity to a business activity. We looked at a list of questions the ATO may ask to help you determine your answer and we quoted the ATO’s definition of what constitutes a business:

“Typically, a business involves a series of continuous and repeated activities that you undertakewith the intention of generating a profit.Profit can take the form of money, but it can also be earned through other means, such as receiving goods or services (such as a barter deal). A one-time transaction may also qualify as a business if it is either:

intended to be repeated

the first step in starting a business.

You can operate one or multiple businesses simultaneously.“

So, given that you may have reviewed your situation and have ascertained that your side hustle is indeed a business, what do you need to do next?

There are several steps you need to take when beginning a business. These are listed below:

Make sure you have a tax file number.

Visit your accountant and ask for help regarding the best structure under which to operate your business. This may be a sole trader, company, trust or partnership or some variation of these structure types.

Register for GST if your GST turnover is or will be, $75,000 over the next 12 months. This can include products or services you’ve received instead of money. Note, if your side hustle is ride-sourcing, you need to register for GST from the day you start, regardless of how much you earn.

Register your business name. This can be done on the ASIC website.

Following on from #5, you will also need to get work cover insurance for your staff. This is state-based so you will need to access this information via your state’s workcover website.

If you intend to pay income tax instalments, register for Pay as you go instalments. You can do this voluntarily or wait for the ATO to tell you when you need to pay instalments.

Depending on the type of business you are running, you may also need to register for Fringe Benefits Tax, Fuel Tax Credits, Wine Equalisation Tax and/or Luxury Car Tax.

Again, depending on your industry, you may need specific state-based licences and council permits. Check with your small business department to find out what you may require.

If you’ve become a director of your company, then obtain a Director ID. Again, your accountant can help you decide if a company structure is appropriate for you.

These are just the basics when starting a new business. There is more to know and do. The best place to start is with your accountant or tax agent. He/she will help guide you through some of these tasks and may even do them for you. Another good place to start is the ATO website – they have a lot of great information to assist you when you are starting a business. Here is their “Before you start a Business” web page. It has loads of useful tips. The ATO also has a series of free courses you can access for new and established businesses – see here.

As the cost of living continues to rise, more individuals are seeking innovative ways to earn extra income on the side. These additional sources of revenue, commonly referred to as “side hustles,” can include anything from mowing lawns for friends and family to selling items on eBay, creating online content, drop-shipping, becoming an influencer, and more. While this supplementary income can be a welcome boost, it’s crucial to understand when you need to report your earnings from your side hustle for tax purposes.

The first step is to determine whether or not you are operating a business. The Australian Taxation Office (ATO) has provided a list of questions that can assist you in making this determination. These questions include:

Do you intend to operate a business?

Do you have the intention and prospect of earning a profit from your activities?

Is the size or scale of your activity sufficient to generate a profit?

Are your activities continuous and repeated?

Are your activities planned, organised, and conducted in a business-like manner? For example, do you:

Keep business records and maintain a separate business bank account?

Advertise and sell your goods and services to the public, rather than just to family or friends?

Operate from business premises?

Maintain any necessary licences or qualifications?

“Typically, a business involves a series of continuous and repeated activities that you undertakewith the intention of generating a profit.Profit can take the form of money, but it can also be earned through other means, such as receiving goods or services (such as a barter deal). A one-time transaction may also qualify as a business if it is either:

intended to be repeated

the first step in starting a business.

You can operate one or multiple businesses simultaneously.“

In essence, if you are attempting to earn a profit from your side hustle, rather than simply supplementing your overall income, there is a strong possibility that you are operating a business. If this applies to you, the next step is to seek advice on your obligations regarding reporting your income and whether or not you need to register for GST and obtain an ABN. We will cover this topic in our next blog.

In this blog I will show you how to set up a fully serviced novated lease for a motor vehicle in Xero. Before I begin, I would like to make it clear that every novated lease arrangement is different, depending on the agreement made between the employee and the lease provider. If this “how to” does not seem to match up with your requirements, please seek further advice from your tax agent or the lease provider. I will not be providing advice to readers about their individual requirements for their novated lease set ups, so please don’t ask! Again, seek advice from your tax professional or the lease provider company if you need help.

What is a Novated Lease?

Before diving into the “how-to” of this blog, it’s important to understand what a novated lease is. A Novated lease itself is a type of vehicle financing arrangement involving an employee, their employer and a leasing provider. Essentially, an employee is able to purchase a vehicle AND receive tax concessions under a salary sacrifice arrangement, orchestrated through payroll. Simply put, “to novate” means “to move with,” and in the context of a novated lease, it signifies that the employee’s vehicle and lease agreement can move with them if they change employers.

How a Novated Lease Works

Basically, a novated lease occurs as per the below steps:

An employee chooses a vehicle to buy.

A Leasing Provider provides a lease agreement to the employee which sees the employer take over the rights and obligations under the lease via a “deed of novation”. It should be noted that the deed of novation includes a clause that transfers the lease obligations back to the employee on termination of the lease or when the employee ceases employment with the employer.

The employee and employer enter into a salary sacrifice agreement whereby deductions are taken from the employee’s pay to fund the lease.

The employer pays the leasing provider with the payroll deduction funds. This means the employer is not out of pocket, both from a cash flow and tax perspective.

What is a Fully Serviced Novated Lease?

In this scenario, another party is introduced – a salary packaging provider. This provider will send the employer a reconciliation report the compares the actual motor vehicle costs against the novated lease estimated costs. If there is any variance, an adjustment must be made to the employee’s pre-tax deduction and sometimes, an adjustment is also required to the post-tax deduction.

A fully serviced novated lease includes, not only the lease repayments, but also other vehicle expenses such as:

Insurance

Maintenance like servicing, repairs and parts

Registration

Fuel

Roadside Assistance

Tolls

Car washing

This type of novated lease operates in the same way as described above, however it has an extra component which is FBT. The post-tax deduction is known as an Employee FBT Contribution which attracts GST. The employer also claims the GST on the novated lease expenses. The pre-tax deduction is calculated as the novated lease expenses minus the post-tax deduction (GST exclusive).

How to Set up the Fully Serviced Novated Lease in Xero

This “how to” will be based on the following novated lease example:

Sonia works for ABC Industries and is paid $120,000 plus super per annum on a monthly pay cycle. She decides to purchase a vehicle costing $60,000 and asks her employer if she can salary sacrifice the purchase via a fully serviced novated lease. Sonia’s employer agrees with the request and asks Billy’s Novated Lease Services to assist with the facilitation of the lease. Once the lease is in place, Billy’s Novated Lease Services provides the following information to ABC Industries:

The novated lease will be for 5 years and based on the following estimated costs, the fixed monthly amount will be $2,017.08. See the details below:

ITEM

GST Exclusive

GST

TOTAL

Lease Payment

14,000

1,400

15,400

Fuel

3,000

300

3,300

Servicing & Repairs

2,000

200

2,200

Registration

900

0

900

Insurance

1000

85

1085

Roadside Assistance

500

50

550

Tolls

400

40

440

Car Wash and Vacuum

300

30

330

TotalEstimated Annual Costs

22,100

2,105

24,205

Monthly Novated Lease Amount

1,841.66

175.42

2,017.08

The fringe benefit figure and related pre and post tax figures are also provided to ABC Industries as below:

The following steps will need to be actioned in order to set up the above lease in Xero:

Step 1 – Add the following accounts to the Chart of Accounts

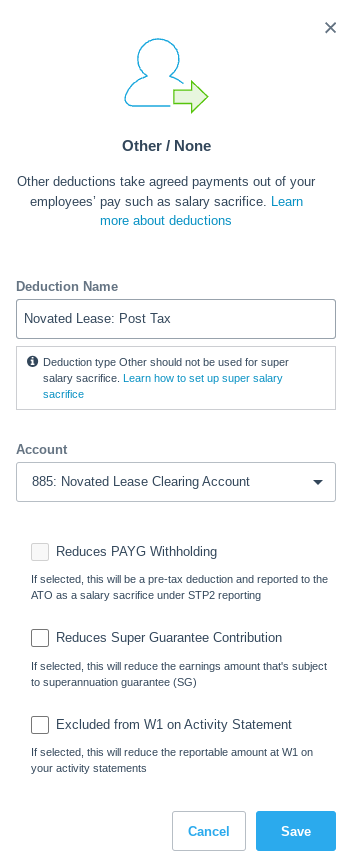

Novated Lease Clearing Account – liability account, current liability; – BAS Excluded tax code; set up a separate account for each affected employee.

Novated Lease Expenses – expense account – BAS Excluded tax code; put under payroll costs like wages or super etc.

Employee FBT Contributions – revenue account – GST on Income tax code; place under non-trading income type e.g. “Other Income”

Fringe Benefits Tax – needed if an FBT liability arises; expense account – BAS Excluded tax code; place under general overheads.

Step 2 – Set up the payroll tax deductions

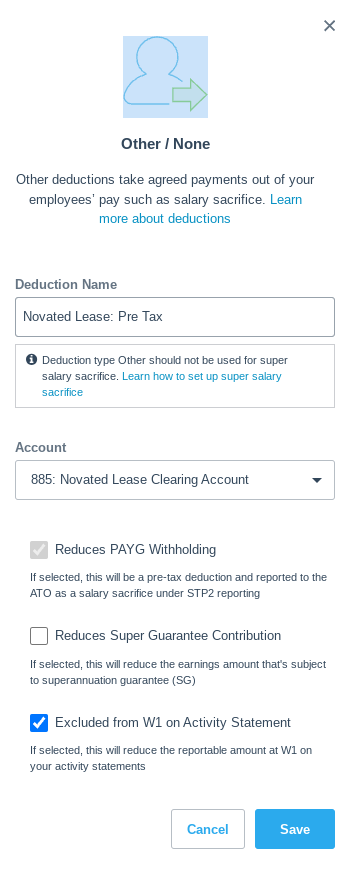

Pre-Tax Novated Lease Deduction – reduces PAYG WH; may or may not reduce SG (but shouldn’t); excluded from W1; STP – Salary Sacrifice – Other Employee Benefits (type O); direct this deduction to the Novated Lease Clearing Account.

Post-Tax Novated Lease Deduction – Does not reduce PAYG WH; Does not reduce SG; Is not excluded from W1; STP – not reportable; direct this deduction to the Novated Lease Clearing Account.

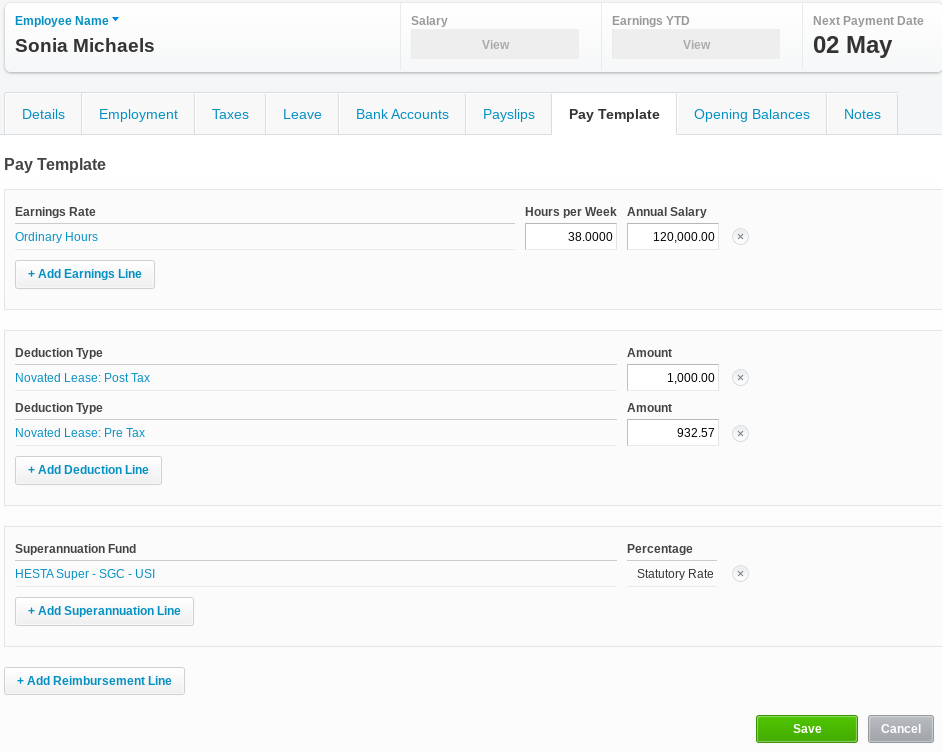

Step 3 – Set up the employee’s pay template & run a pay cycle

Open Sonia’s pay profile in Xero. Add the two deductions as above, then enter the figures provided by the lease provider. See below:

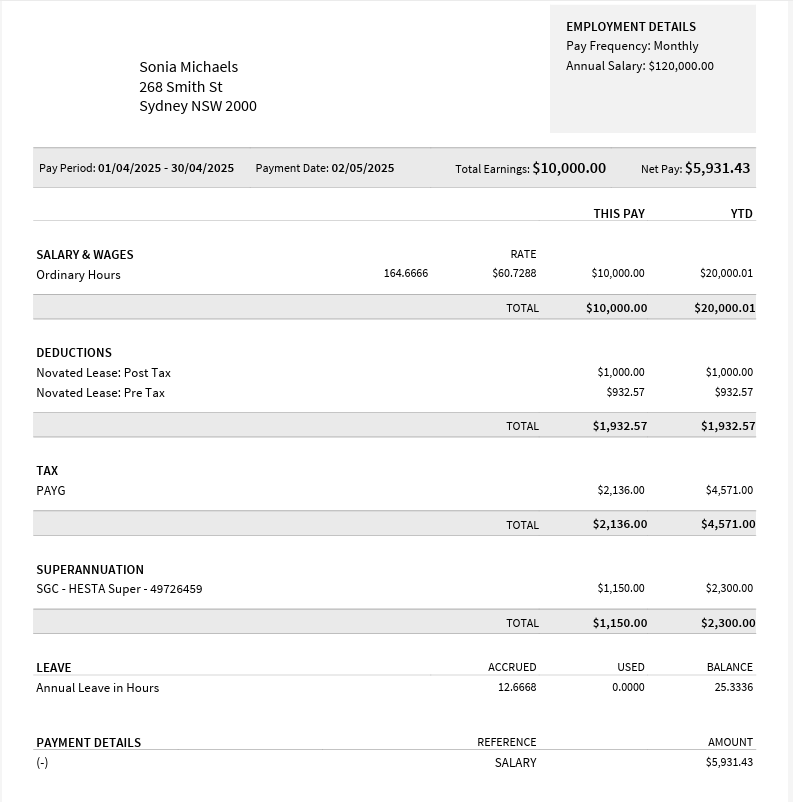

Now process the April pay run in Xero. Sonia’s payslip should look like the below example:

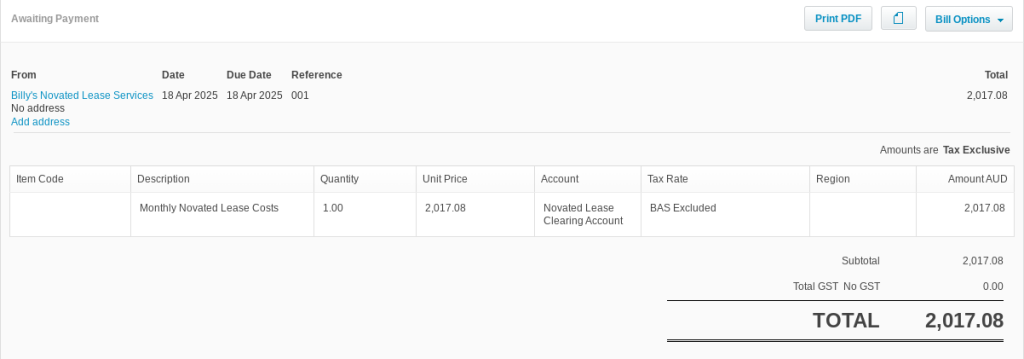

Step 4 – Record the lease provider’s invoice in Xero

In Xero, add the invoice received from the lease provider, “Billy’s Novated Lease Services”. Post the invoice to the Novated Lease Clearing Account with the BAS Excluded tax code. See an example below.

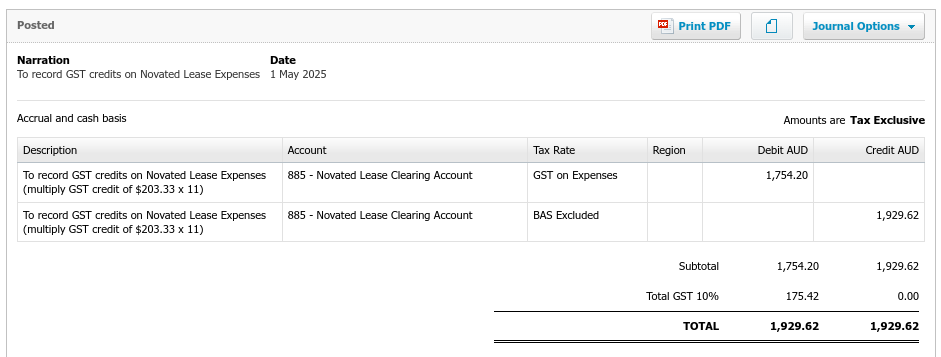

Step 5 – Record GST

There are two GST-related transactions to bring to account:

GST on the novated lease expenses

GST on the post-tax deduction

Each month, Billy’s Novated Lease Services will send ABC Industries a report detailing any GST credits available from the novated lease arrangement from the previous month. For ease of explaining this “how to”, we will assume the GST credits align with the example data. The GST credit therefore is $175.42. Now multiply the GST by 11. This will give rise to a figure of $1,929.62. To recognise the GST from the monthly report, enter the following journal:

Here, GST of $175.42 will move to the GST control account and become claimable in the BAS. The clearing account will receive net credit of $175.42.

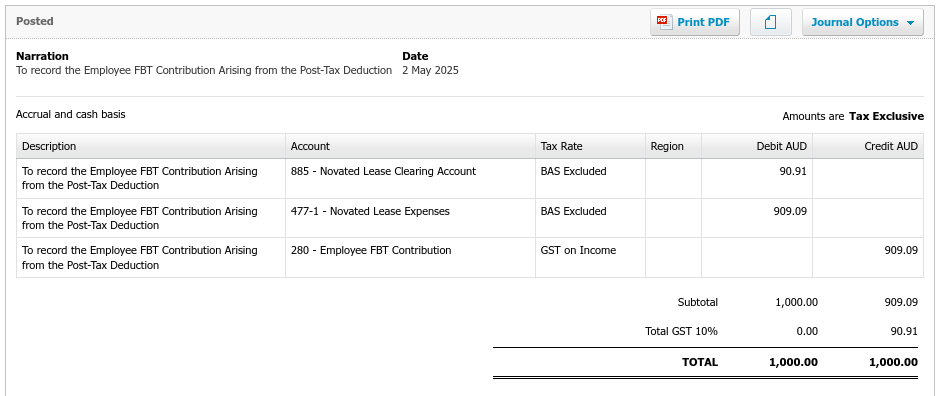

In order to take up the GST from the post-tax novated lease deduction i.e $90.91, enter the following journal:

The consequences of this journal will be:

$90.91 is credited to the GST control account;

The Novated Lease Clearing Account receives a debit of $90.91; and

Novated Lease Expenses receives a debit of $909.09.

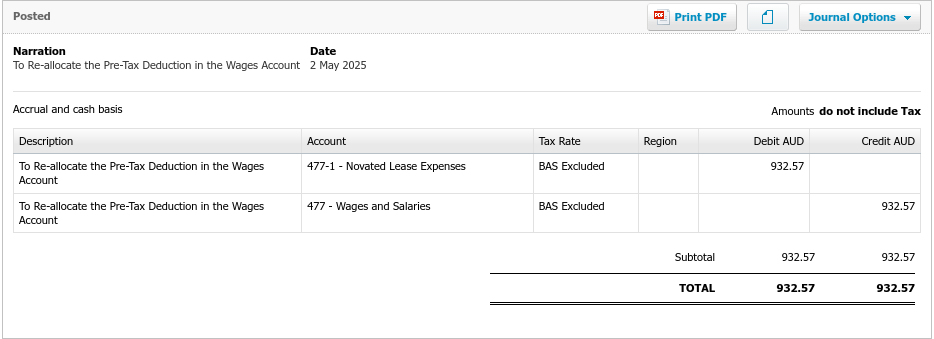

Step 6 – Correct overstated wages

The above payroll event has resulted in overstating the gross wages in the profit and loss. This is corrected by entering the following journal:

Behind the scenes – how are the accounts and the BAS affected by the novated lease?

Now that the above transactions have been processed in Xero, it would be prudent to show you how they affect the accounts and the BAS. Firstly, the novated lease clearing account has been cleared to zero as can be seen below. The account should return to zero each month after the payroll has been processed. If it doesn’t, you will need to investigate to find the cause!

The profit and loss shows the employee FBT contribution as other income and the lease and wage expenses are listed as expected:

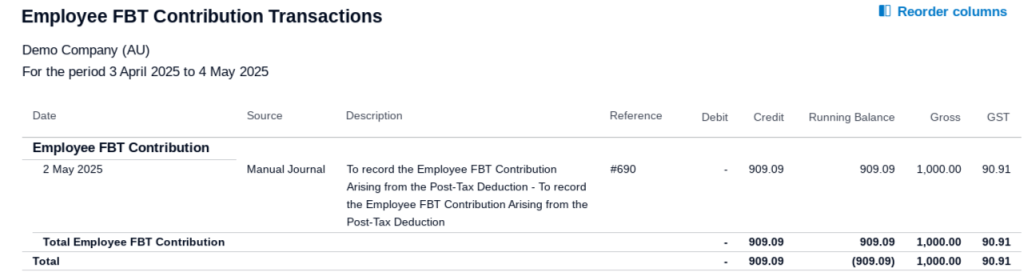

Now let’s drill into each profit and loss account to see the details. Looking at the FBT income I recorded at step 5, we can clearly see the GST posted of $90.91.

Next we can see the details behind the novated lease expenses recorded at step 5 and step 6. The total agrees with the monthly GST exclusive expense amount estimated by the lease provider.

Lastly, looking behind the wages expense transactions, we can clearly see how the wages are reduced by the reallocation of the pre-tax deduction:

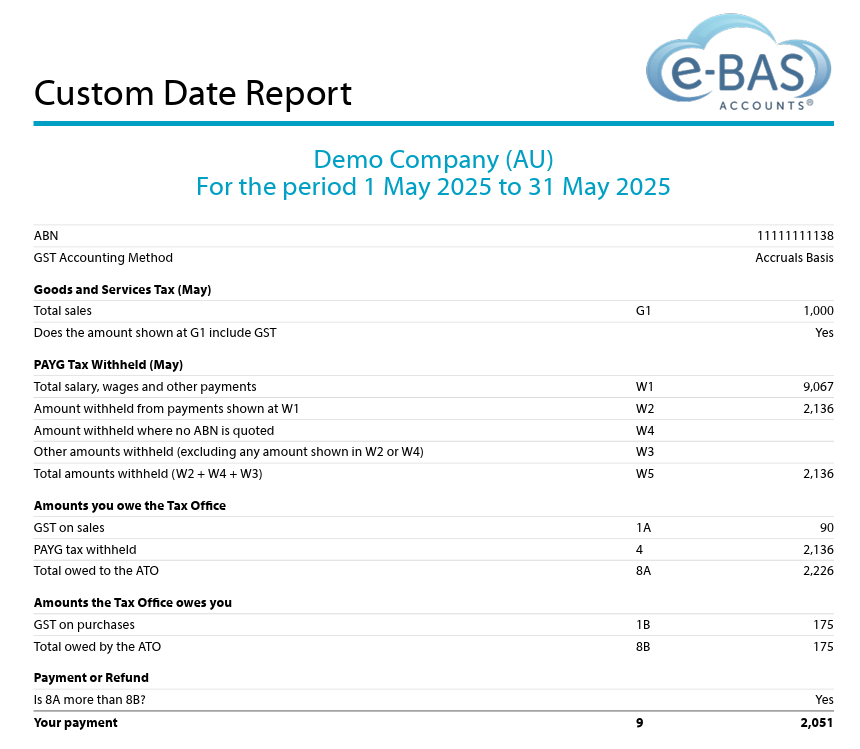

Now we will take a look at the BAS. Note the GST on sales of $90 from the FBT contribution and the GST on Purchases of $175 from the novated lease expenses journal. Also note the reduced gross wages figure which is the correct figure to report to the ATO.

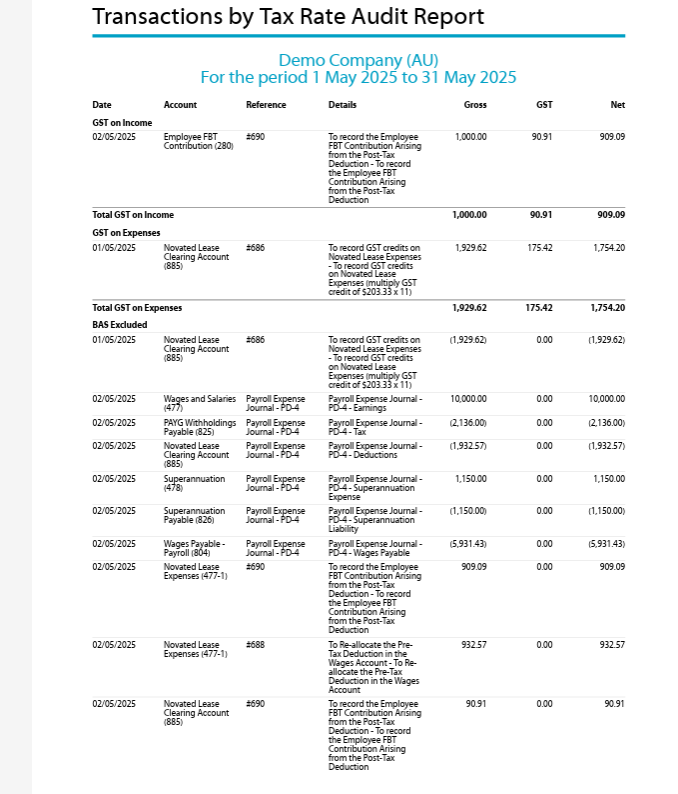

Drilling down into each GST type below, shows us the origin of the figures:

Summary

Setting up a fully serviced novated lease in Xero, as outlined in this guide, offers one approach to managing these arrangements. It’s important to remember that variations in novated lease structures exist, each with its own implications for employee wages and payroll processing. While the data you receive from your lease provider might differ from the steps detailed here, this ‘how-to’ should provide a solid foundation for establishing the necessary accounts and configuring tax deductions within Xero. Please note that I cannot offer guidance on your specific lease agreement, however, I’m happy to address any questions you have about the instructions provided in this blog. Finally, the example figures used in this guide are purely illustrative and should not be evaluated for their financial accuracy or feasibility. The primary goal here is to demonstrate the mechanics of setting up a novated lease within Xero, so please focus on the procedural steps rather than the example’s specific details.

New Criminal Underpayment Laws began on 1 January 2025. It is now an offence to underpay your staff. If found guilty, you may face hefty fines or jail time, or both. Read on to find out what these laws mean and how you can avoid a conviction going forward.

What are these laws?

Employers found to be intentionally underpaying staff by Fair Work, will be investigated. If a case can be raised, it will be referred for criminal prosecution. If an employer is convicted, he/she may face prison time and/or fines (see below).

Employers who have made an honest mistake and did not intend to underpay staff, will not be prosecuted.

How to protect yourself

Fair Work has created the Voluntary Small Business Wage Compliance Code. This Code can be used to check if you are paying your staff correctly. Employers who have complied with the Code in relation to an underpayment, cannot be referred for possible criminal prosecution by Fair Work. Therefore, if you suspect that you may have underpaid staff, it is in your best interests to review the above Code ASAP!

Another way to protect yourself is to write an Cooperation Agreement. This is an agreement between Fair Work and an employer that outlines a possible underpayment event. While the agreement is in force, Fair Work cannot refer the matter for possible criminal prosecution, however, civil enforcement may apply regardless.

Which fines and prison time can apply?

For a company

If the court can determine the amount of the employer’s underpayment, the maximum fine will be the higher of:

3 times the amount of the underpayment

$8.25 million.

If the court can’t determine the amount of the underpayment, the maximum fine is $8.25 million.

For an individual

The court can impose a maximum of 10 years in prison or a fine, or both.

If the court can determine the amount of the employer’s underpayment, the maximum fine will be the higher of:

3 times the amount of the underpayment

$1.65 million.

If the court can’t determine the underpayment, the maximum fine is $1.65 million.

How to avoid all of the above

Simple really! Good employers do two things:

1. Stay up to date with payroll obligations including changes to awards, legislation and employees’ circumstances such as their roles, duties, classifications, relevant qualifications, age, hours of work or location of work.

2. Reach out to reliable sources for help when difficult payroll situations arise. These may include bookkeepers, tax agents, payroll HR associations, payroll processing services, industrial associations and Fair Work.

If you are reading this and are concerned about your situation, now might be the time to reach out to your tax professional and ask for assistance. Fair Work mean business!!

Late edit:

Fair Work have released their long awaited Payroll Remediation Guide. You can download it here. This Guide is directed more to larger employers, where a large number of underpayments or number of impacted employees are identified, or where the issues detected are complex and involve multiple industrial instruments.

Payday Super is coming! Payday Super aims to stop employers from not paying employees super or paying it late. The premise is that super will need to be paid after each pay run, even termination pay runs. Payday Super is set to begin from 1 July 2026.

Two proposed models for Payday Super implementation are:

“Employment payment” model: Employers must pay SG contributions on the same day as wages.

“Due date” model: SG contributions must reach the superannuation fund within a specified time after payday.

Both depend on the definition of “payday,” which includes any payment with an ordinary time earnings component, even outside the regular pay cycle like termination payments or bonuses. SG contributions would be calculated based on the ordinary time earnings paid on payday.

Payday Super will have specific impacts on the Super Guarantee Charge process and the maximum contribution base calculations. The government will consult with key stakeholders and the public to ensure these impacts are minimal.

The Government will finalise the Payday Super framework in the 2024–25 Budget. Legislation will be introduced for the measure set to begin on 1 July 2026. The ATO is consulting and co-designing with digital service providers for implementation.

In the meantime, employers must consider how Payday Super will affect their payroll processes and cash flow. It is also important to note that by July 2026, the super rate will be 12% which will also impact business cash flow. There are lots of issues to consider here and I will keep you updated as more information about Payday Super comes to hand.

Note: The government has released draft legislation to mandate payday super, a policy that was first flagged in the 2023-24 Federal Budget.

The ATO has decided that small businesses with a history of non-payment, late or non-lodgement or incorrect reporting, will be moved from quarterly to monthly GST reporting i.e. a monthly BAS.

The ATO will begin this process from 1 April 2025 and will start with around 3,500 small businesses (and no, this is not an April’s Fool joke!). Those businesses affected will need to remain on the monthly cycle for a minimum of 12 months.

The ATO believes that this new protocol will help small businesses to comply with their tax obligations because they will need to be more organised in terms of bookkeeping to lodge a monthly BAS. The ATO also thinks that this will assist cash flow given business owners will need to pay smaller amounts more regularly.

If small business owners continue to ignore their tax debts and compliance obligations, it is not a question of “if” but “when” they will hear from the ATO. From the ATO Deputy Commissioner, Will Day:

‘We take our role seriously and are committed to supporting viable small businesses to comply with their ATO obligations, while also taking firmer action on those who are deliberately not complying to ensure they aren’t getting an unfair advantage. If you’re a small business who continues to deliberately disregard your obligations, you can expect the ATO to move you to more frequent GST reporting’.

The ATO will contact small business owners and their tax professionals if BAS reporting needs to move to a monthly cycle. There will be a review process in place for those small business owners who believe they do not have a history of non-compliance.

If you own a small business and are non-compliant, expect to move to monthly BAS lodgements soon. Contact your tax professional or the ATO ASAP to discuss, as the impact on your business finances and processes will be significant!

My Thoughts

I fully support the ATO’s efforts to recover long-standing tax debts and understand that non-compliance gives some an unfair advantage over those who follow the rules. However, this protocol might worsen the situation for some small business owners. Here are some issues I believe may arise from this ATO campaign:

Monthly BAS lodgers must lodge and pay by the 21st of each month, losing the extension given to quarterly online lodgers, who get an extra month. While this could encourage better organisation in bookkeeping and cash flow, it might also lead to more disorganisation and increased tax debt for some. A better idea perhaps, would be to allow business owners to remain on a quarterly cycle but disallow the lodgement extension. That way, they are still forced to be more organised and pay more regularly, but without the onerous task of doing so monthly.

Those business owners on a current ATO payment arrangement may need to re-negotiate if they are expected to pay a monthly BAS on top of other tax debt. This is because all current and future BAS must be paid on time in order to retain the payment arrangement. This may be quite difficult for some, but I guess this is what the ATO are trying to achieve – pulling in tax revenue more regularly and on time.

Businesses using tax professionals will face higher costs, paying for 12 BAS lodgements per year instead of 4. This increase in bookkeeping/accounting fees will add further financial stress. Some business owners might choose to handle it themselves to save money. While this works for those familiar with accounting, it could result in messy accounts and BAS reporting errors for others.

As a bookkeeper/BAS Agent, I’ve noticed that non-compliant clients are often not great business owners. They are disorganised and need constant reminders, which is already challenging on a quarterly cycle. Doing this monthly would be even more frustrating, likely leading to strained relationships and parting ways with clients.

I hope the ATO has considered these implications. While monthly reporting might help some, it could increase financial stress and non-compliance for others.

I do believe some business owners shouldn’t be in business, especially those who think they’re above the law. In my opinion, they should be closed down and made to repay their debts over time. This ATO measure might help, but perhaps more decisive action, like forced business closure (or the threat thereof), is needed.

You may have heard that Payday Super is coming in July 2026. In short, Payday Super will require all employers to pay their employees’ super on the same day as a pay run is processed. The main reason behind this measure is that the Government wishes to end non-payment and underpayment of super by some employers as this is effectively wage theft. The measure will also mean that millions of employees will receive higher retirement savings due to their super contributions being paid earlier and more frequently.

What you may not know is that from 1 July 2026, the ATO Small Business Super Clearing House (SBSCH) will close. Yes, you heard right—it is closing its doors at the same time as Payday Super begins.

So, what can you do to prepare if you are a current SBSCH user? Your options are limited. You can either move to your default super fund’s clearing house or use the super functionality in your payroll software, such as Xero, MYOB, or QBO. I recommend not waiting until the SBSCH closes to get this organised. Make the change as soon as practicable.

How did I hear about the SBSCH closing? I read the fact sheet from the Government Treasury website. You can access the fact sheet here if you wish to read the details behind Payday Super.

The fact sheet breaks down many other details about Payday Super and is an important read if you are an employer. I suggest you take the time to review it and figure out how you will apply this change to your payroll processes when the time comes.